Wiring the future: how Nexans is cashing in on the electrification boom

If you’ve ever wondered what keeps the world’s lights on, factories humming and data centers running, the answer is often hidden in plain sight: cables. As the global push for electrification accelerates, the humble cable has become a linchpin of modern life, quietly powering everything from electric vehicles to AI-driven data centers. At the heart of this transformation is Nexans a company with a reach that now spans the globe.

Nexans is the backbone behind the energy transition, connecting continents, cities and critical infrastructure with their advanced cable systems. Whether it’s bringing offshore wind power to shore, upgrading aging grids, or enabling the next wave of smart buildings, Nexans is right there, often unseen but always essential.

In this article, we’ll break down what makes Nexans tick, how they make their money, who really owns the company, and why they might just be one of the most interesting (and underappreciated) stocks in the energy sector today. Let’s plug in and see what’s really powering the future.

Powering the future: who is Nexans?

The energy sector is the foundation of modern industrial society. A stable and efficient electricity transmission system is essential for everything from manufacturing and transportation to digital infrastructure. In recent years, demand for electricity has risen sharply, driven by the growing number of electric vehicles, the electrification of heating systems and the rapid expansion of data centers for artificial intelligence. As the global economy becomes increasingly electrified, the importance of resilient and intelligent energy transmission networks is growing.

One company that plays a key role in this development is Nexans. Founded in 1879 and headquartered in Paris, the company brings more than 140 years of experience to the cable industry. Today, Nexans operates in 41 countries and runs more than 60 production facilities worldwide. Its products and services are a central part of the ongoing transformation of the global energy system.

To understand Nexans’ business, it is helpful to look at the company’s role in the energy value chain. Nexans designs, manufactures and installs cable systems for a wide range of applications, including long-distance transmission lines, medium and low voltage cables for regional networks and wiring systems for buildings and infrastructure projects. In addition to its physical products, Nexans provides planning, installation support and long-term maintenance services, which are especially important in complex environments such as offshore wind farms or cross-border energy connections beneath the sea.

What sets Nexans apart is its ability to combine deep technical knowledge with the practical execution of large-scale infrastructure projects. The company has built its reputation on providing high quality cable systems that meet the demanding requirements of energy transmission and distribution. Nexans supports clients throughout the entire project lifecycle, from system design and planning to installation and operational maintenance. This integrated approach has helped position the company as a reliable partner for public utilities, grid operators and private developers of energy infrastructure.

Nexans generates the largest portion of its revenue in Europe, accounting for about 45 percent of total sales. Key markets include France, Germany and Norway. North America contributes about 22 percent, with Canada playing a particularly important role. The rest of the company’s revenue comes from Latin America (13 percent), Asia (12 percent) and Africa (8 percent). This broad international presence reflects both the company’s European roots and its ambition to support energy projects globally.

How Nexans makes money: inside the product engine

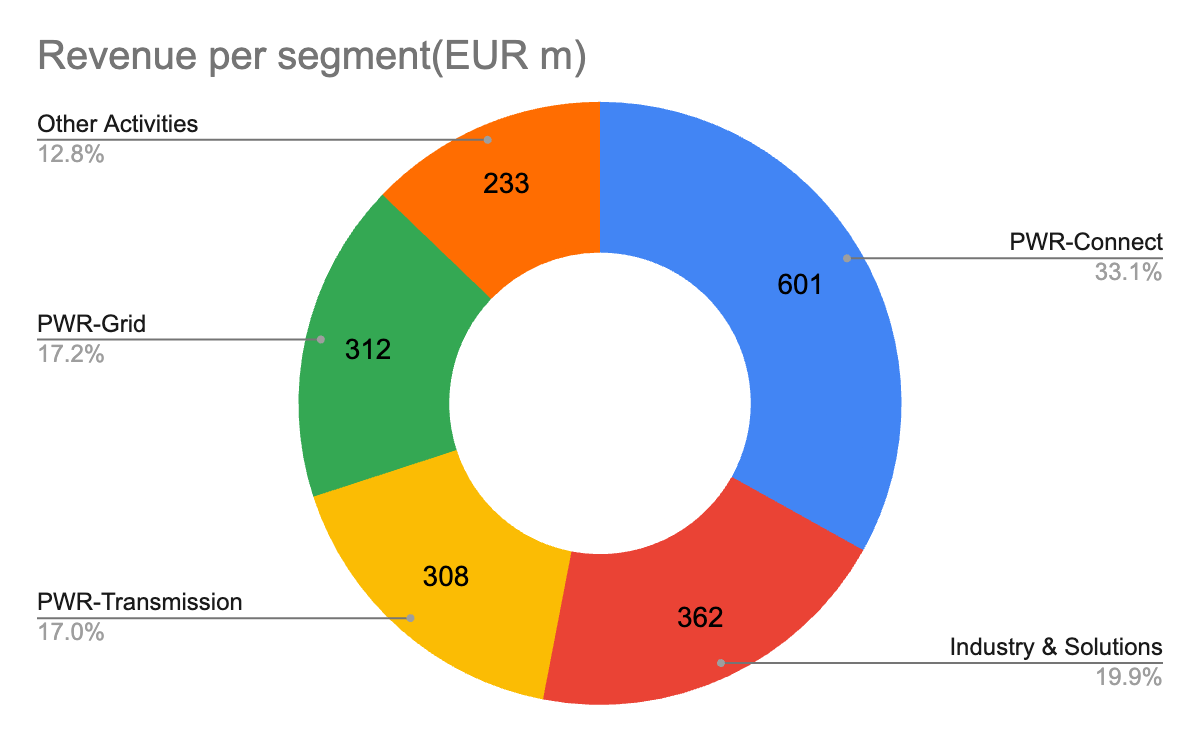

To better understand how Nexans generates its revenue, it is useful to take a closer look at the company’s operating segments. Nexans divides its business into five main areas, three of which fall under Electrification. These three segments are responsible for the majority of the group’s revenue and reflect the company’s strategic focus on energy infrastructure.

The first segment is Power Transmission. It accounts for around 17 percent of total revenue and includes the development and production of high voltage cable systems. These cables, which often operate at several hundred kilovolts, are designed to transport electricity across long distances. They are used to connect offshore wind farms or nuclear power plants with major consumption centers. Customers include transmission system operators, utilities and governments seeking to link power grids through interconnectors. These projects often extend across borders and are implemented both on land and underwater.

Q1 2025 brought in €308 million in sales with 21.7% organic growth. This growth has been rock-solid for five years and forecasts through 2030 look just as strong.

The numbers tell the story. Q1 2025 brought in €308 million in sales with a solid 21.7% organic growth.

They are sitting on an €8.1 billion backlog that keeps them busy until 2028. They are also adding their third cable-laying ship, the Nexans Electra, in 2026. This segment is catching the energy transition wave at the right time.

The second segment, Power Grid, also contributes 17 percent of total revenue. This area focuses on medium and low voltage cables, typically operating between one and thirty kilovolts. These cables deliver electricity from the main grid into cities, towns and rural areas. The core customers are distribution system operators who manage local and regional power networks. Nexans produces aluminum cables and related accessories, serving as a crucial link between national energy infrastructure and end users.

Most grids in Europe and the US are over 40 years old and need upgrades. This creates steady demand for Nexans. The company reports strong order intake, especially in Europe and the Middle East/Africa, driven by renewable energy projects and grid upgrades.

Nexans has a robust electrification backlog with a high percentage of future sales already locked in through 2028.

Note: 2020-2022 figures aren't disclosed by the company. These are forecasts based on segment growth rates and electrification market trends.

The third and most important segment is Power Connect. It represents approximately 33 percent of revenue and covers very low voltage cables used inside buildings and infrastructure. These cables carry electricity from distribution panels to sockets, lighting systems and electrical appliances. This business unit primarily serves electrical contractors, construction firms, building operators and developers of infrastructure such as charging stations for electric vehicles. Nexans places a strong emphasis on premium solutions, focusing on quality, durability and safety.

The segment grew 1.9% organically in Q1 2025. Canada, South America and the Middle East performed well, while Europe lagged due to weak housing demand. But that's likely temporary.

Note: 2020-2022 figures aren't disclosed by the company. These are forecasts based on segment growth rates and electrification market trends.

There is strong momentum with premium customers. The focus on high-value fire safety cables and smart installation solutions suggests a healthy pipeline ahead. Recent acquisitions like La Triveneta Cavi and Reka Cables should boost both the backlog and growth prospects.

In addition to these core segments, Nexans operates a division called Industry and Solutions. This area lies outside the traditional electrification value chain and includes specialized cable systems for industries such as automation and rail transport. Although smaller in scale, it adds valuable diversification and taps into markets with distinct technical requirements.

The final category, Other Activities, includes the sale of raw copper wire. This segment is of limited strategic relevance and does not play a central role in Nexans’ long-term positioning.

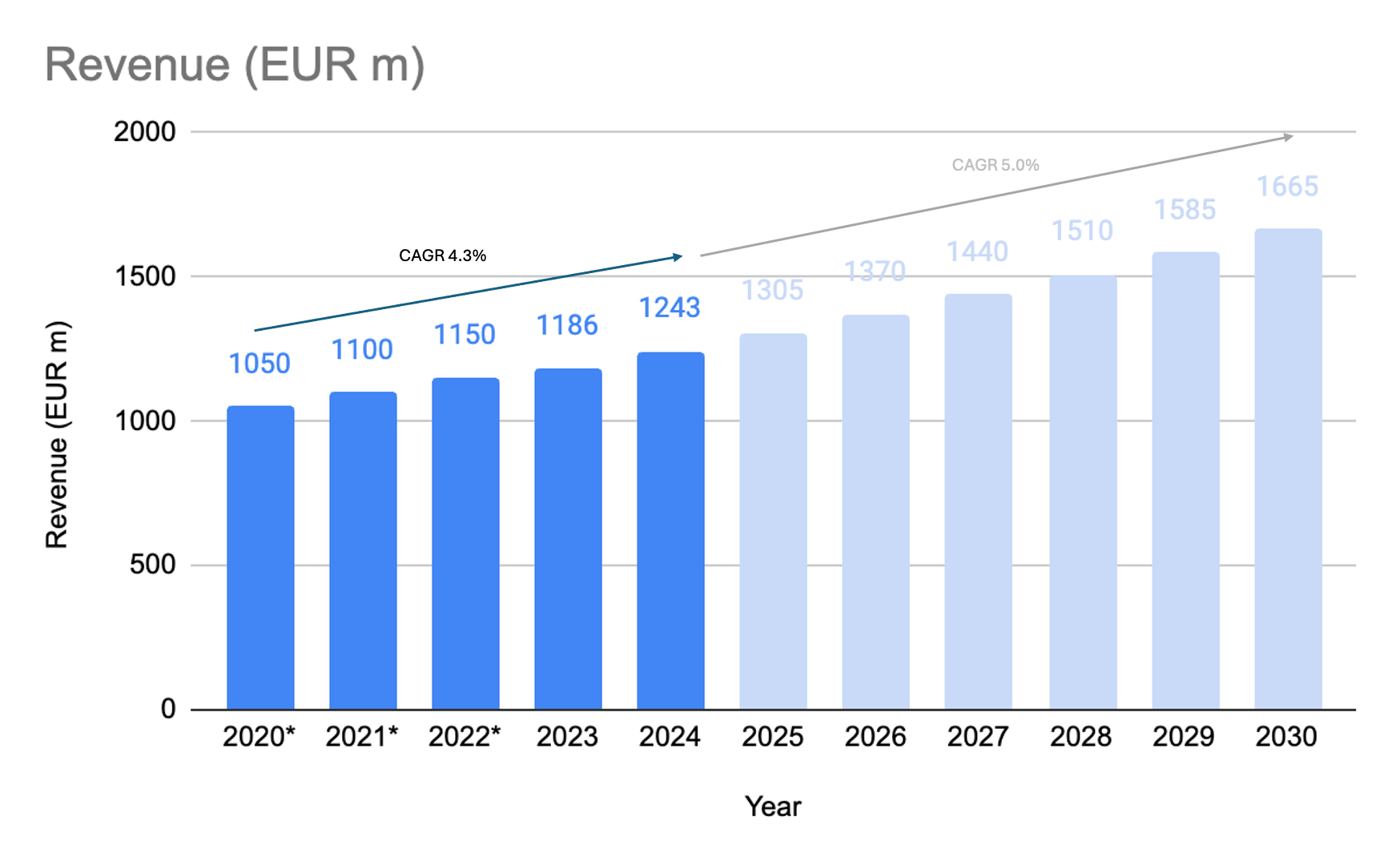

Looking at future growth potential, the company targets organic revenue growth in the range of three to five percent per year. Profit growth is expected to be in a similar mid-single-digit range. Given the capital intensity and competitive nature of the industry, this level of growth reflects a focus on operational efficiency and selective project execution rather than aggressive expansion.

Who really owns Nexans? A Look at the shareholder roster

The ownership structure of Nexans provides insight into the company’s strategic orientation and long-term interests. A significant portion of shares is held by Invexans Ltd., a subsidiary of the Chilean industrial conglomerate Quiñenco. With a stake of just over 14 percent, Invexans is not merely a financial investor but a long-term partner, represented on the board of directors and supporting Nexans in its international strategy and transformation toward electrification.

Another notable shareholder is Baillie Gifford, which holds nearly 8 percent of the company. Based in Edinburgh, this investment firm is known for its long-term approach and focus on companies with strong growth potential. The presence of such a shareholder reflects a belief in the structural relevance of Nexans and its ability to participate in the global energy transition.

Bpifrance Participations, the investment arm of the French public development bank, owns slightly more than 5 percent of the shares. Its involvement is noteworthy because Bpifrance typically invests in companies considered strategically important to the French economy. The decision to take a stake in Nexans suggests the French government views the company as systemically relevant to the country’s energy infrastructure and resilience.

The remaining shares are broadly held by institutional and private investors. Institutional investors make up the largest group, while private individuals and employees hold smaller portions. The management team owns only a minimal number of shares. Overall, Nexans is predominantly owned by institutions, with very limited insider ownership.

How Nexans stacks up: rivals, market position, and a real-world SWOT

Nexans operates in a highly competitive market shaped by technological complexity, cyclical investment patterns and growing global demand for electricity infrastructure. The energy transition has created a structural need for new grid capacity to support renewables and rising consumption from electric mobility and digital infrastructure. This demand is accelerating, but it is also attracting a wide range of competitors.

Among Nexans’ most notable rivals are Prysmian, based in Italy and NKT, headquartered in Denmark. Both are active globally and serve similar markets. Prysmian is the largest company in the cable industry and benefits from economies of scale and a broad product portfolio. NKT has a strong presence in Central and Northern Europe and, like Nexans, focuses on technically advanced high voltage solutions. In more standardized cable segments, competition is price-driven and intense, making it harder to defend margins. However, in specialized areas such as subsea connections or high voltage direct current transmission, barriers to entry are higher and experience matters more. This is where Nexans is able to differentiate itself.

Still, the overall market remains challenging. Large-scale projects are often awarded through competitive tender processes, putting pressure on pricing and requiring strong capabilities in financing, planning and execution. New players are emerging from adjacent industries such as renewable energy, data infrastructure and battery storage. For Nexans, deep technical expertise is no longer sufficient on its own. Strategic positioning, regulatory awareness and the ability to form long-term partnerships are increasingly important.

Despite these challenges, the long-term outlook is positive. The global expansion of electricity networks is a multi-decade transformation. Companies that can deliver quality at scale and maintain trust with utilities, governments and infrastructure developers will be well positioned. Nexans has the experience, technological capabilities and focus to compete in this evolving landscape.

Let us now take a step back and look at the company through a SWOT analysis to summarize where Nexans currently stands.

Wired for growth: big trends shaping Nexans’ future

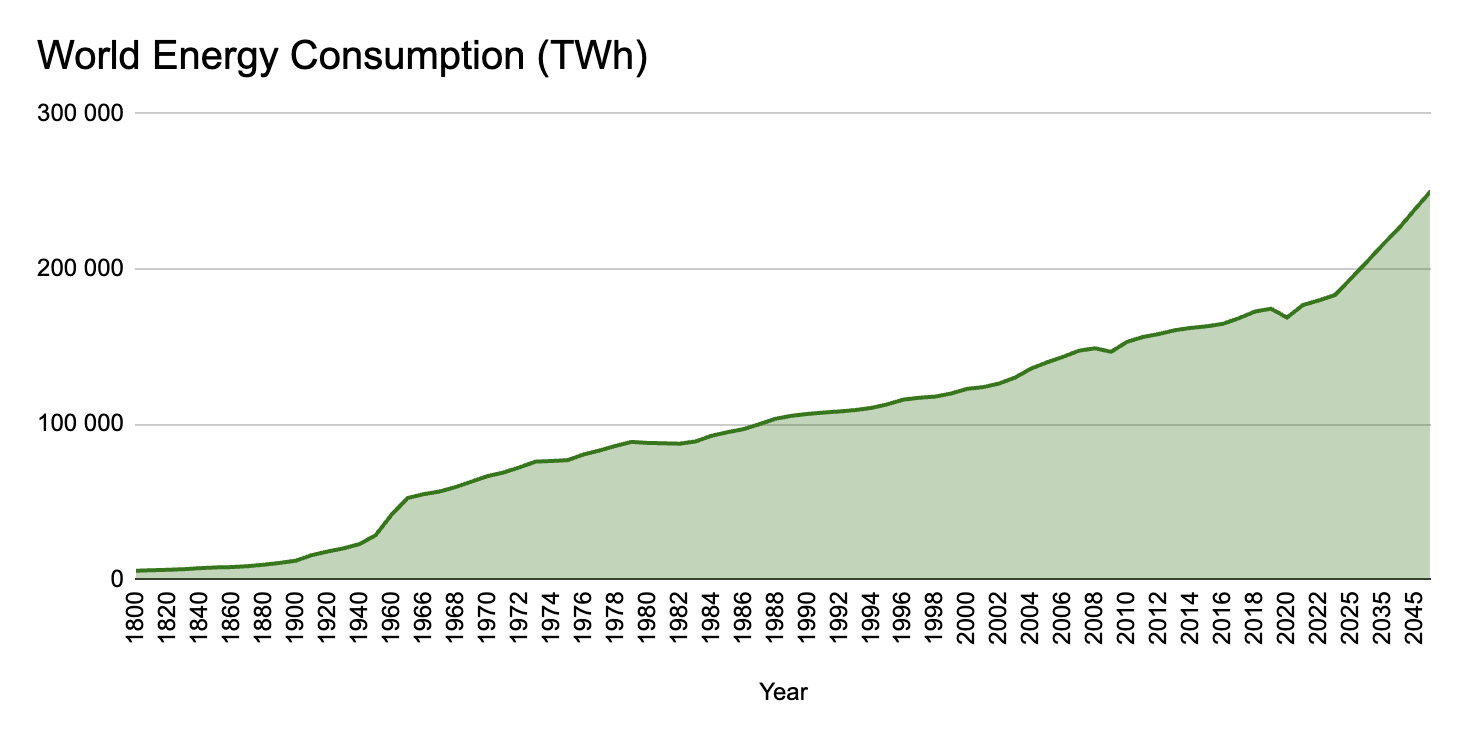

The long-term outlook for the global cable industry is shaped by powerful structural trends. By the year 2050, total energy consumption is expected to increase by nearly 50 percent.

This surge is driven by the rapid adoption of electric vehicles, the growing energy needs of data centers powered by artificial intelligence, the ongoing industrialization of emerging economies and sustained global population growth. Electricity is set to play an increasingly central role in the energy mix. While it currently accounts for around 20 percent of global energy consumption, this share is projected to rise to more than 30 percent over the coming decades.

These developments present major opportunities for companies like Nexans, but also logistical challenges. Renewable energy sources, such as wind and solar, are decentralized. Unlike in the past, when conventional power plants were built close to population centers, renewable installations are often far from where electricity is consumed. Offshore wind farms can generate large amounts of energy but are often hundreds of kilometers away from industrial hubs or urban areas. Many renewable assets are directly connected to local distribution networks rather than high-voltage grids, increasing the complexity and volume of required infrastructure.

As a result, the modernization and expansion of both transmission and distribution networks will become a central task in the global energy transition. Industry forecasts expect the market for cables to grow by approximately 7 percent per year until 2028. Over the same period, global electricity demand is projected to rise significantly. Meeting this demand will require not only new generation capacity, but also the physical systems that connect supply and consumption.

In response, Nexans is targeting steady growth. The company aims to increase its total revenue by around 5 percent annually through 2028. Within its core electrification business, the target is an organic growth rate between 3 and 5 percent per year. Given the scale of global investment required in power infrastructure, these objectives appear both realistic and strategically aligned with broader market dynamics.

Inventing the next grid: Nexans’ R&D edge

Grid modernization and efficient operation require innovative solutions. Nexans invests €140 million annually in R&D (2% of sales) focusing on five key areas:

High-voltage & subsea cables: 525kV DC cables and dynamic cables for floating offshore wind farms that are critical for connecting renewables.

Smart grid solutions: AI-powered monitoring and predictive maintenance tools like Adaptix.Grid.

Fire safety & low-carbon cables: greener cables with recycled materials for critical infrastructure.

Easy-install products: faster installation cables plus digital tools for installers.

Recycling solutions: cable recycling and carbon tracking to help customers meet sustainability goals.

Recent launches include Fire Safety cables, Mobiway Un'Reel packaging and AI-powered grid monitoring.

What could go wrong? The real risks for Nexans

There are real business risks, but Nexans actively manages them with smart strategies.

Raw material price swings: Nexans depends heavily on copper, aluminum and polymers. Price spikes or supply shortages squeeze margins fast.

Nexans’ response: long-term supplier contracts, financial hedging, diversified suppliers and internal recycling facilities.

Project execution problems: complex infrastructure projects face delays, technical issues and cost overruns leading to penalties.

Nexans’ response: selective project criteria, rigorous management systems, thorough risk assessments and experienced partnerships.

Economic slowdowns: recessions delay or cancel infrastructure projects.

Nexans’ response: geographic/market diversification, cycle-resistant high-value solutions and strong balance sheet with low debt.

Competitive pressure: price wars in the competitive cable market erode margins.

Nexans’ response: heavy R&D investment, strong customer relationships, operational efficiency improvements and strategic acquisitions.

Regulatory & sustainability risks: new environmental rules or ESG failures create costs, contract losses and reputation damage.

Nexans’ response: robust compliance programs, low-carbon investments, transparent ESG reporting and relevant certifications.

Why Nexans stays ahead: the moats that matter

These advantages are not unbreachable, but they should protect margins and market share over time.

High switching costs: big customers like utilities can't easily change cable suppliers without re-qualifying products, retraining staff and risking project delays. Once Nexans is embedded, customers rarely switch mid-project.

Scale advantage: as one of the world's largest cable companies, Nexans gets better supplier pricing, spreads R&D costs wider and handles international projects smaller players can't touch.

Technical leadership: heavy R&D investment creates specialized solutions that command premium prices. They lead in high-voltage subsea cables for offshore wind, expertise most competitors lack.

Trusted brand: in critical infrastructure where failure isn't an option, customers pay premiums for proven reliability. Utilities choose Nexans knowing cables will meet high standards and last decades.

Data network effects: more smart cable installations generate better data, improving solutions and attracting more customers.

Financial analysis

Business quality: getting better with time

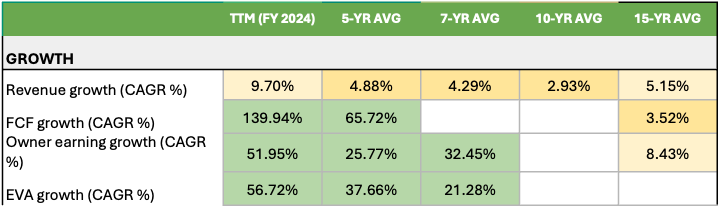

Nexans' numbers tell a story I really like. This company has been steadily improving over the past decade.

Profitability is rising: the company has dramatically improved at converting sales into actual profits. Management is clearly getting better at running the business. Gross margins have also strengthened, showing they're successfully moving away from low-margin commodity products toward higher-value solutions.

Cash generation is strong: free cash flow has more than doubled compared to recent years. For a capital-heavy business like this, generating strong cash flow is impressive and shows they're creating real value, not just paper profits.

Returns look good: return on Equity has improved significantly and is now quite respectable for an industrial company. The steady climb over many years shows consistent improvement in how efficiently they use shareholder capital.

My take: these trends show genuine business quality improvement over time.

Growth: hitting the accelerator

Revenue growth is accelerating: revenue growth has nearly doubled compared to recent averages. Their electrification strategy is clearly paying off after years of modest performance.

Cash flow growth is eye-popping: free cash flow growth has been explosive, showing they're not just growing revenue but converting that growth into actual cash at an accelerating rate.

Profitability growth is outstanding: owner earnings growth demonstrates the quality of their expansion is improving. They're getting bigger and more profitable simultaneously, which is exactly what you want to see.

What I find encouraging: cash flow and profitability are growing faster than revenue, meaning they're becoming more efficient as they scale.

Bottom line: Nexans transformed from steady plodder to growth machine.

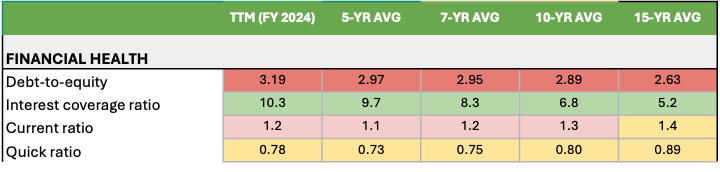

Financial health: solid but not perfect

Debt levels: higher but manageable: debt levels have increased as they invest in growth projects and acquisitions. However, their ability to service debt has actually improved significantly, showing earnings growth is outpacing borrowing costs.

Liquidity: adequate but tight: short-term liquidity is workable but not generous. They can meet obligations, though there's limited cushion. This suggests they're running a tighter operation and being aggressive about deploying capital.

My take: they're borrowing to fund growth, which makes sense given the opportunities. Financial health is solid but worth monitoring.

Management: learning to allocate capital

Asset efficiency is improving: management has gotten dramatically better at generating profits from the company's asset base. The improvement has been consistent across multiple time periods, proving this isn't just luck.

Capital returns are strong: returns on invested capital are solid and have improved steadily over many years. Cash returns on capital are particularly impressive, suggesting they're generating strong real returns on investments.

Shareholder returns: balanced approach: dividend yield has increased modestly while share buybacks remain minimal. This makes sense given the growth opportunities ahead - why waste money on buybacks when you can invest in higher-return projects?

Here's my verdict: the consistent improvement across multiple metrics gives me confidence they know what they're doing and are focusing on the right priorities.

Valuation

Current Metrics:

Share Price: EUR 97.25 (as of 2025-06-23)

Net Cash Per Share: EUR 27.87

Net Asset Value: EUR 40.71

Liquidation Value: EUR 167.18

Scenario Analysis (15% Required Return, 20% margin of safety):

Scenario 1 (Conservative):

Assumption: 2% initial growth declining to 0.50% terminal rate

Intrinsic Value: EUR 81.10

Verdict: Overvalued by 19.92%

Scenario 2 (Realistic):

Assumption: 4% initial growth declining to 1% terminal rate

Intrinsic Value: EUR 86.91

Verdict: Overvalued by 11.89%

Scenario 3 (Optimistic):

Assumption: 8% initial growth declining to 2% terminal rate

Intrinsic Value: EUR 101.25

Verdict: Undervalued by 3.95%

Our take: is Nexans worth a spot in your portfolio?

After digging into the numbers, strategy and market trends, we think Nexans stands out as a rare mix of old-school industrial know-how and forward-looking innovation. The company is riding some of the biggest global trends: electrification, renewable energy and digital infrastructure. Nexans is winning major projects, locking in long-term backlogs and steadily shifting its business toward higher-value and more resilient segments.

Sure, there are risks: raw material swings, project hiccups, and tough competition. But management seems to be learning fast, getting more efficient and investing where it counts. The balance sheet is solid, cash flow is strong and the company’s moats (technical expertise, scale and customer trust) are real.

For retail investors looking for exposure to the energy transition without betting on the next hot tech stock, Nexans offers something different: steady growth, improving profitability and a business that’s absolutely essential to the world’s future. In our opinion, Nexans deserves a closer look. It’s not flashy, but sometimes the best investments are the ones quietly powering everything else.

| A guest post by

|