Why This Biotech Outlier Could Be the Next Big Value Play

This company stands out as a global leader in antibody innovation, with a proven track record of scientific breakthroughs, successful product launches, and strategic partnerships with major pharmaceutical players.

For paid subscribers: company details, financial analysis and valuation is at the end of the article

Introduction of the Company

Founding and Evolution

The company was founded in 1999 in Denmark with a vision to harness antibody science for transformative therapies targeting cancer and other serious diseases. In its early years, the company focused on developing fully human monoclonal antibodies — a field that was just emerging at the time. Over the past 25 years, the company has evolved from a small Danish biotech into a global leader in antibody innovation, now operating across North America, Europe, and Asia Pacific. This growth has been driven by scientific breakthroughs, strategic collaborations, and successful product launches, establishing the company as a key player in the biotechnology sector.

What the Company Does

At its core, the company is on a mission to make a real difference for patients by creating innovative antibody medicines. The goal for 2030 is to deliver “knock-your-socks-off” (KYSO) therapies for cancer and other serious diseases. The company’s values — passion, innovation, collaboration, and integrity —are showing up in everything from research to partnerships to patient care.

The business model is pretty straightforward: discover, develop, and bring to market new antibody-based therapies. The company leans on its own proprietary technology platforms — like DuoBody (for bispecific antibodies), HexaBody (for enhanced immune function) and ADCs (antibody-drug conjugates) — to build a strong pipeline of unique products. By mixing in-house R&D with strategic partnerships, the company can push its own programs forward while teaming up with big pharma to get its discoveries out to more patients.

Where does the money come from?

Royalties: ongoing payments from partners (like J&J, Novartis)

Net Product Sales: direct sales of the company’s own medicines (like EPKINLY)

Collaboration Revenue: upfront, milestone, and profit-sharing from partnerships

License Fees: payments for using the company’s technology

Reimbursement Revenue: R&D cost reimbursements from partners

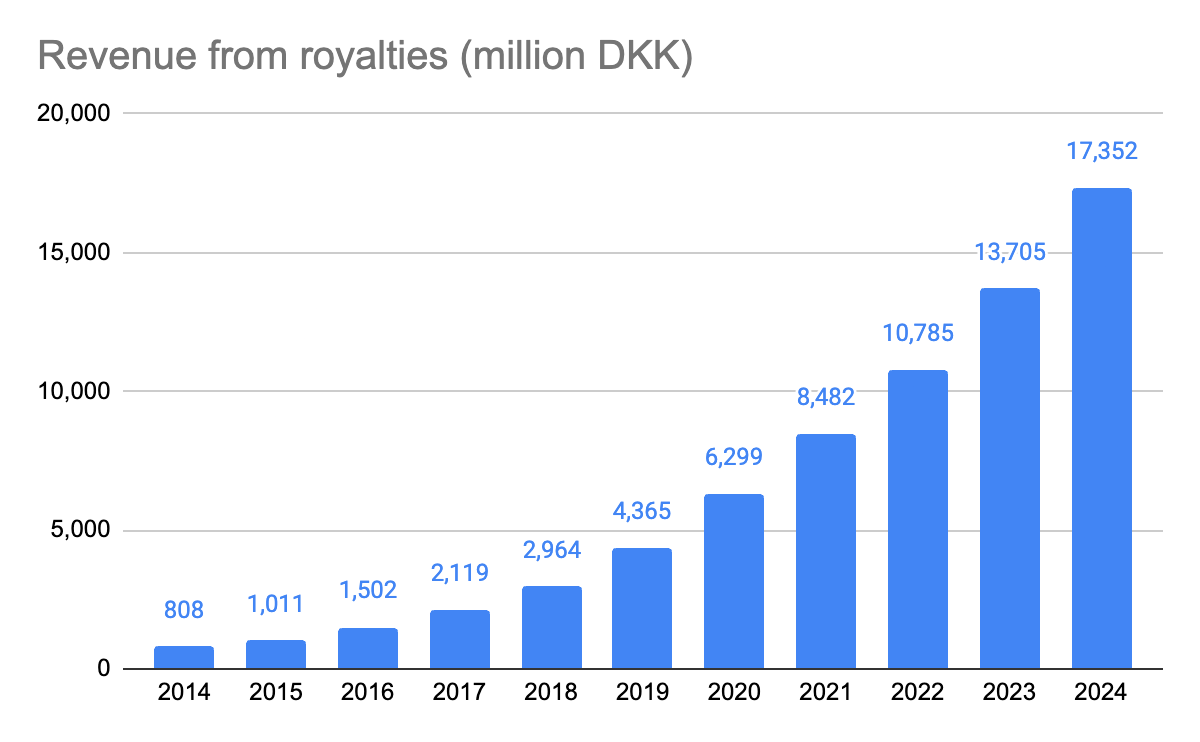

Revenue growth has been impressive over the last 10 years with CAGR 37.93%.

Largest revenue is coming from royalty payments.

Global Footprint

The has a truly global presence with teams spread across Denmark, the Netherlands, the US, Japan, and more.

Headquarters:

Copenhagen, Denmark: the main HQ and research hub

Regional Offices:

Utrecht, Netherlands: major European R&D center

Princeton, New Jersey, USA: North American HQ, handling clinical development, regulatory, and commercial work

Tokyo, Japan: overseeing activities in Japan and the Asia Pacific region

Other Global Moves:

The company’s products and tech are commercialized worldwide through partnerships with big names like Johnson & Johnson, Novartis, AbbVie, Seagen/Pfizer, and BioNTech.

Clinical trials are happening in multiple countries, showing just how global the company’s approach is.

Who Owns the Company?

Most of the shares are in the hands of big institutional investors (over 60–70%). Insiders (management and board) usually own less than 5%, and the rest is held by retail and other investors.

The Biotech Sector Outlook (2025–2030)

I am working on a detailed research on the sector available soon, but here is a short overview of the market to put the company’s operation into context.

The global biotech market is on a roll, expected to grow with CAGR 8–12% through 2030. By then, the sector could top $1.5 trillion in annual revenue, thanks to innovation, aging populations, and rising healthcare needs.

What’s driving this growth?

Cancer and immune diseases are still the biggest and fastest-growing areas, with antibody therapies, cell and gene therapies, and personalized medicine leading the way.

Antibody engineering (like bispecifics and ADCs) is taking off, with more approvals on the horizon.

Precision medicine, powered by genomics, AI, and big data, is making treatments more personal and effective.

An aging world means more chronic diseases—and more demand for new therapies.

Emerging markets in Asia-Pacific, Latin America, and the Middle East are investing heavily in biotech.

Digital health is merging with biotech, opening up new ways to care for patients and develop drugs.

Trends to watch:

More partnerships and M&A as companies look to expand their pipelines and tech.

Regulators are streamlining approval for breakthrough and rare disease drugs.

ESG (environmental, social, governance) is becoming a bigger deal for investors.

But there are challenges:

Drug development is still risky, lengthy and expensive, with lots of failures along the way. A typical product development cycle looks like this:

Pressure to keep drug prices in check could squeeze profits.

Competition is fierce, especially in hot areas like antibodies and cell therapies.

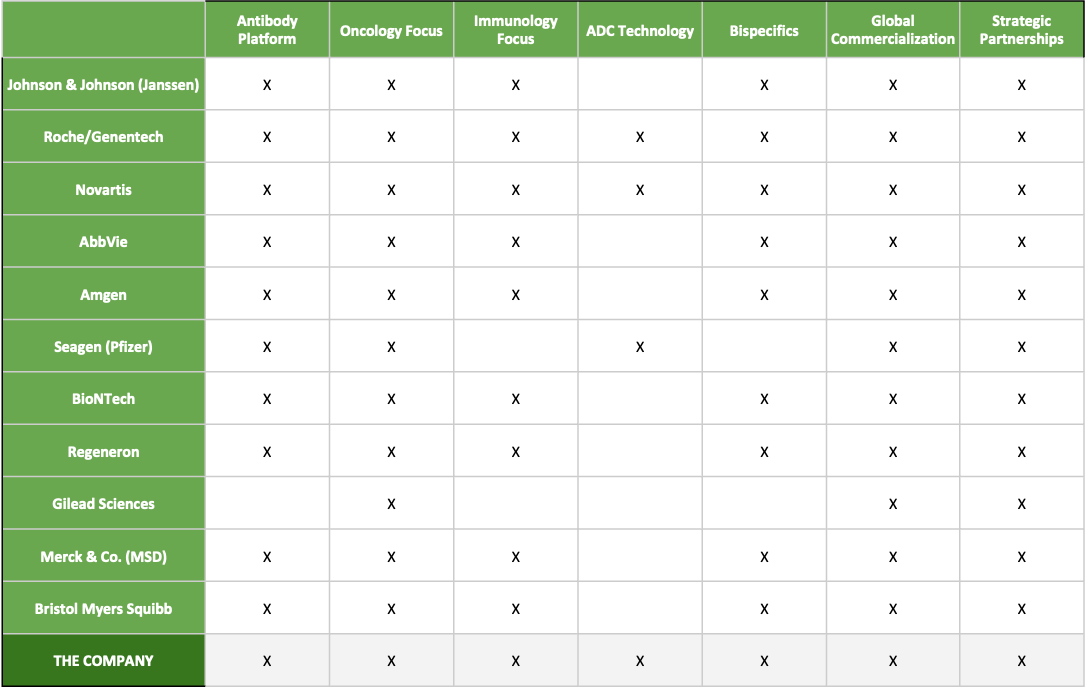

How the Company Stacks Up

The company is seen as a global leader in antibody innovation, especially in cancer, and its commercial presence keeps growing.

Innovation: Proprietary platforms like DuoBody®, HexaBody®, and ADCs keep the company at the cutting edge.

Commercial Success: Big royalties from partnered products and rising direct sales of new therapies.

Pipeline: Deep and diverse, with next-gen antibody drugs and late-stage assets.

Partnerships: Collaborations with major pharma boost global reach and share the risk.

Financial Strength: Steady revenue growth, high R&D spending, and a solid balance sheet.

The company is a “mid-to-large cap” biotech, competing with both big pharma and other innovative biotechs, and is known for scientific rigor, successful launches, and monetizing its tech through both sales and partnerships.

Deep Dive Into the Business Operations

Product development

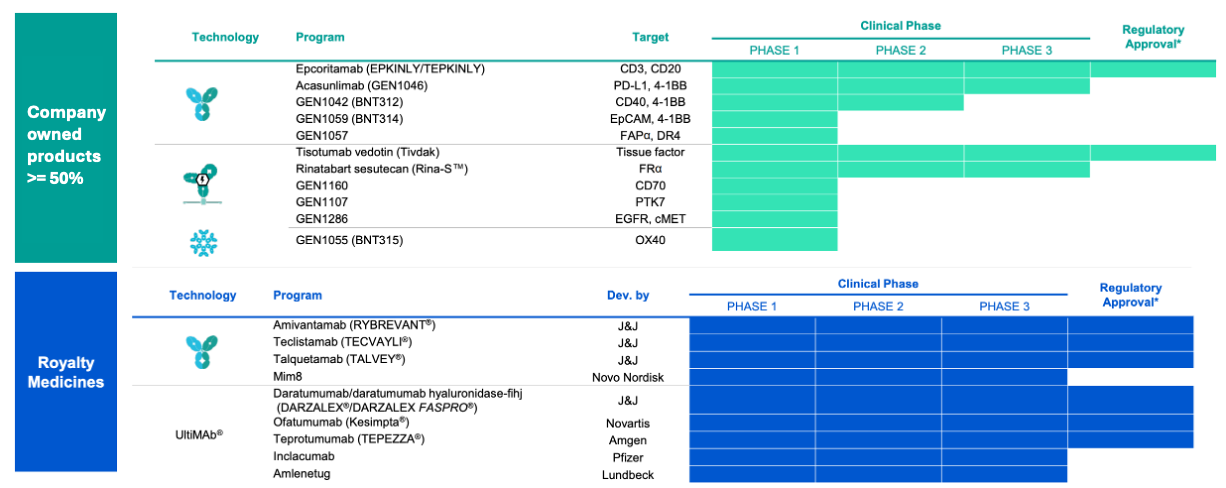

The company is serious about product development, investing about 60–62% of revenue into R&D. The pipeline is robust, covering everything from early discovery to late-stage clinical trials:

Royalties

The biggest chunk comes from royalties, mainly from products sold by partners. In 2024, royalties brought in DKK 17,352 million (about 81% of total revenue), with a CAGR of 35.89%.

Most of the royalty revenue comes from Johnson and Johnson through DARZALEX product and Novartis through Kesimpta product

The royalty portfolio is strong and set to grow further with new product introduction: Mim8 (phase 3 filing expected in 2025), Inclacumab, Amlenetug (phase3 potential filing is “near”)

** the company is entitled to royalty in US until 2029 and 2031 in rest of the world

Product sales

In 2024, net product sales hit DKK 1,743 million (about 8% of revenue), including direct sales of the company’s own products. Recent product launches are showing strong growth, and there are promising late-stage candidates in the pipeline set to boost the sales further.

Tivdak (profit share with Seagen/Pfizer) product was launched in late 2021 with fast growing sales (DKK100 million ($63m) in 2022 and DKK500 million ($131m) in 2024, which is CAGR 44.2%)

EPKINLY/TEPKINLY product had a strong launch (2023) performance

(DKK 421m ($64m) in 2023 and DKK 1,743m ($281m) in 2024, which is a 339% growth).

Market potential of the product is very strong.

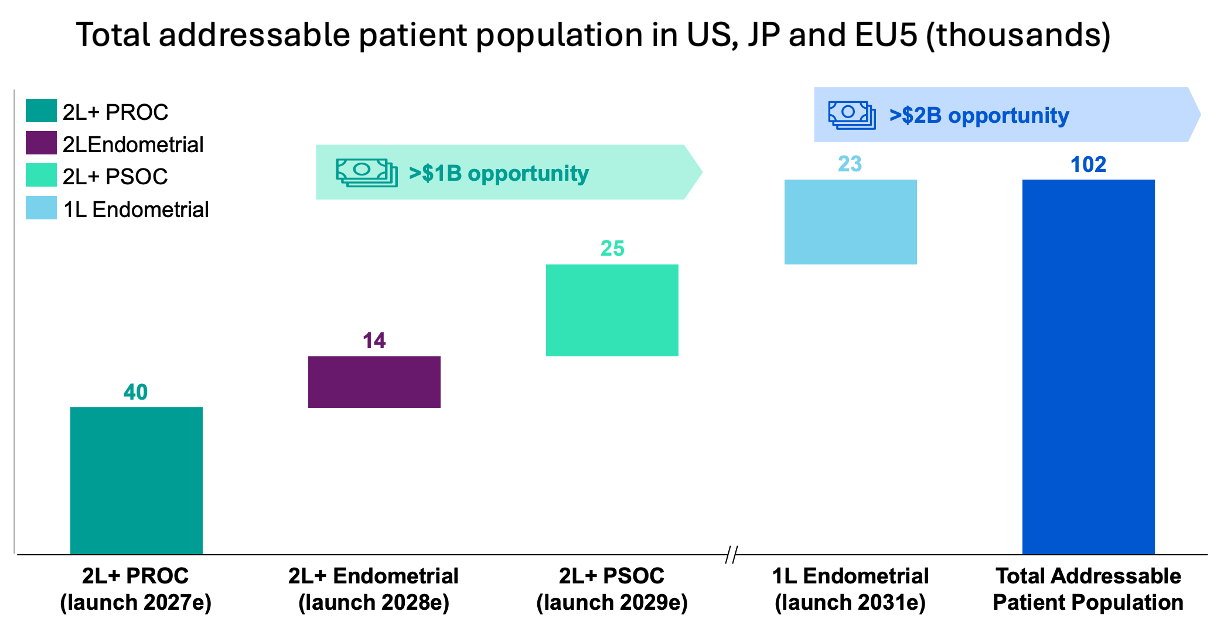

The company has two late-stage products in the pipeline, also with strong market potential:

Rina-S: Overian and endometrical cancer

Acasunlimab: Potential First-in-class Bispecific for CPI-exposed Solid Tumors

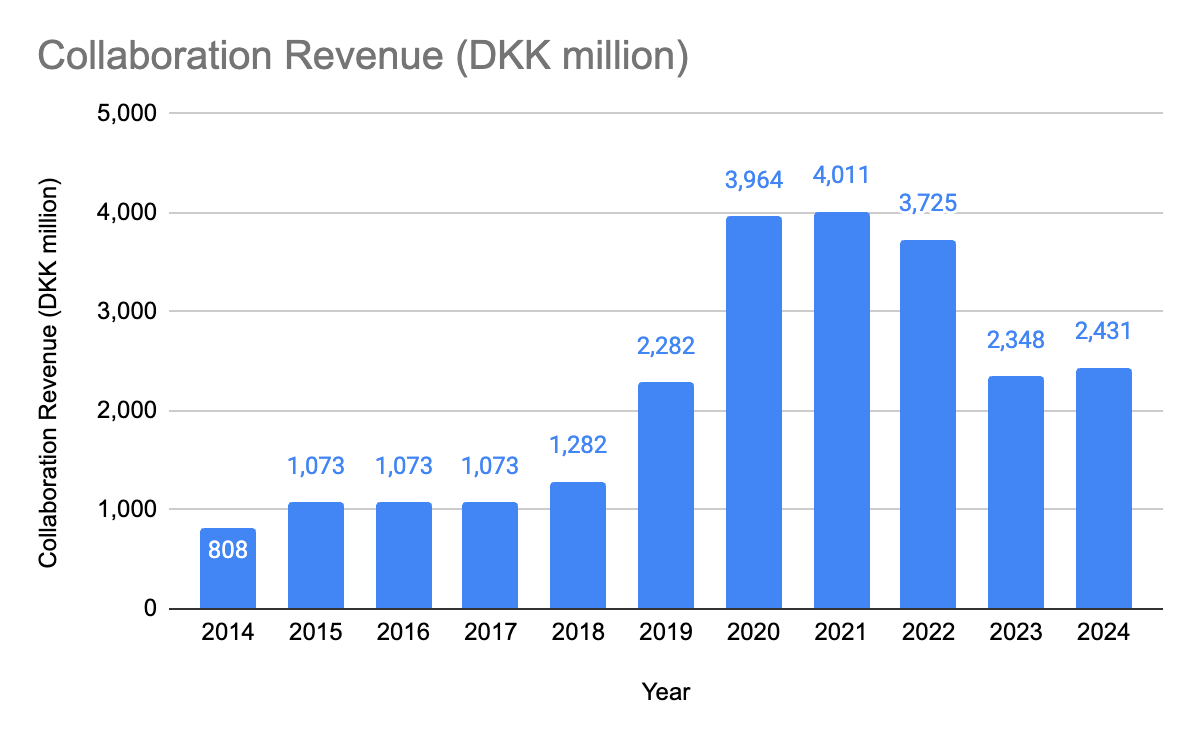

Collaboration

This includes upfront payments, milestones, and profit-sharing from co-development and commercialization deals. In 2024, collaboration revenue was DKK 2,431 million (about 11% of revenue), with a CAGR of 11.64%. This stream can be a bit lumpy, depending on when milestones are hit and new deals are signed.

Payments from partners such as AbbVie, BioNTech.

Why Have Collaboration Revenues Dropped?

Fewer Big Milestone Payments: collaboration revenue depends a lot on hitting certain R&D, regulatory, or commercial milestones in the company’s partnered projects. In 2021 and 2022, there were several major milestone payments as key products (like EPKINLY and Tivdak) moved forward or got approved. But in 2023 and 2024, there just weren’t as many big milestones reached, so milestone income was lower.

Not as Many New Upfront Payments: when the company signs a major new partnership or licensing deal, it usually gets a big upfront payment. The last couple of years saw fewer of these large new deals compared to 2020–2022, when the company landed some high-value partnerships (like those with AbbVie and BioNTech).

More Focus on Product Sales: the company’s business model is shifting, with more revenue now coming from direct product sales (like EPKINLY and Tivdak) and royalties (especially from DARZALEX and Kesimpta). As these areas grow, collaboration revenue naturally becomes a smaller slice of the overall pie.

Year-to-Year Ups and Downs: collaboration revenue is always a bit unpredictable and can swing a lot from year to year, depending on when milestones are hit or new deals are signed. This kind of volatility is pretty normal for biotech companies with lots of partnerships.

What’s Fueling the Company’s Growth?

A Deep, Innovative Pipeline & R&D Power

The real engine behind the company’s growth is its relentless focus on research and development. Year after year, the company reinvests more than 60% of its revenue back into R&D — an impressive commitment that keeps the discovery and development of next-generation antibody therapies moving full speed ahead. Thanks to proprietary technology platforms like DuoBody®, HexaBody®, and ADCs (antibody-drug conjugates), the company is able to create unique treatments that tackle tough diseases, especially in oncology.

The pipeline isn’t just deep—it’s broad, covering everything from early discovery to late-stage clinical trials. Some of the standout assets include:

EPCORE® (epcoritamab): A bispecific antibody for B-cell cancers, with multiple ongoing trials in different types of lymphoma.

Tivdak® (tisotumab vedotin-tftv): An antibody-drug conjugate for cervical cancer, co-developed with Pfizer/Seagen, and now being tested for other solid tumors.

Emerging assets: The company is also advancing a range of next-gen bispecifics, immune checkpoint modulators, and ADCs, both on its own and with partners.

The 2024 acquisition of ProfoundBio added even more firepower, bringing in new ADC candidates and boosting the company’s capabilities in solid tumors. This constant innovation means the company is well-positioned for long-term growth, with new product launches and smart management of existing assets.

Strategic Partnerships & Collaborations

Teaming up with the right partners is a huge part of the company’s success story. The company has a knack for forming win-win alliances with some of the world’s biggest pharma players—think Johnson & Johnson, Novartis, AbbVie, Pfizer/Seagen, and BioNTech.

These partnerships bring a lot to the table:

Global reach: Partners like J&J and Novartis have massive sales and marketing networks, helping the company’s products reach more patients worldwide.

Shared risk: Co-development deals mean the company doesn’t have to shoulder all the financial and operational risks alone, while still benefiting from milestone payments, royalties, and profit-sharing.

Faster progress: Joint research, tech licensing, and shared expertise help speed up the development of promising new therapies.

Recent deals—like the co-development of EPCORE® with AbbVie and the collaboration with BioNTech on next-gen immunotherapies—show just how good the company is at attracting top-tier partners and blending outside innovation with its own R&D.

Expanding Markets & New Opportunities

Growth isn’t just about new drugs—it’s also about reaching more patients in more places. The company already has a strong commercial presence in the U.S., Europe, and Japan, and is eyeing new markets in Asia-Pacific and Latin America, where demand for cutting-edge cancer therapies is rising fast.

There’s also big potential in expanding the use of existing drugs. Many lead assets, like EPCORE® and Tivdak®, are being tested in multiple cancer types and treatment settings. If clinical trials go well, these drugs could be approved for more uses, opening up bigger markets and more revenue.

And the company isn’t stopping at cancer. Ongoing investment in new antibody formats, ADCs, and immune cell engagers could unlock new treatments for autoimmune diseases and rare disorders.

What Sets the Company Apart (The Moat)

Proprietary Antibody Tech: unique platforms make it tough for competitors to copy. It is a strong moat.

Deep Pipeline: lots of products in the works, so the company isn’t betting everything on one drug. This is a partial moat as some other players also have deep pipeline

Strategic Partnerships: big pharma partners mean more reach and shared risk. This is a partial moat as strategic partnerships are industry trends. The the quality of partners which matters the most and the company is strong in that.

Strong Patents: a wide patent portfolio protects the company’s innovations. This is a strong moat.

Risks to Watch

The major risks an investor must be aware of:

Clinical and Development Risk: drug development is risky — project / product development failures could hit financials hard.

Regulatory Risk: delays or denials from regulators can throw off timelines delaying revenues and increasing cost base at the same time.

Market Risk: competition is fierce, and pricing pressures are real.

Partnership Risk: relying on partners for commercialization and revenue can be tricky. The company is mitigating this risk by shifting gradually to direct sales.