Vopak: A Contrarian's Bet on Global Trade and Energy Storage

If you're seeking a high-quality infrastructure play with exposure to the global energy transition, Vopak might be the perfect fit. In this article, I will break down in details Vopak's business model, competitive advantages, and financial performance to see if it's a worthwhile addition to your portfolio.

Company: Royal Vopak

Symbol:

VPK.ASExchange: Euronext Amsterdam (Netherlands)

Market cap: $5 bn

Company overview

Vopak, headquartered in the Netherlands, is a leading independent tank storage company. It has evolved into a global player specializing in the storage and handling of liquid bulk products, including chemicals, oil, gases, and new energies. Vopak is recognized for its strong commitment to safety, sustainability, and operational excellence.

What Vopak Does

Vopak's core business is the storage and handling of liquid bulk products. The company owns and operates a global network of strategically located terminals in key ports and industrial clusters. In addition to its core business, Vopak provides value-added services for its clients.

The company generates revenue from the following activities:

Storage Fees: long-term contracts for tank storage capacity.

Handling/Throughput Services: fees for product movement, blending, and conditioning.

Value-Added Services: heating, cooling, nitrogen blanketing, and quality management.

Logistics & Ancillary Services: pipeline, barge, rail, and truck logistics, plus customs and documentation.

New Energies & Sustainable Feedstocks: storage and handling of hydrogen, ammonia, CO₂, and biofuels.

Joint Ventures & Associates: share of profits from co-owned terminals.

Other Income: rental, asset sales, and miscellaneous services.

Vopak operates the following types of terminals:

The company’s value proposition is built on its ability to offer safe, reliable, and efficient storage solutions, supported by advanced technology and a strong commitment to sustainability.

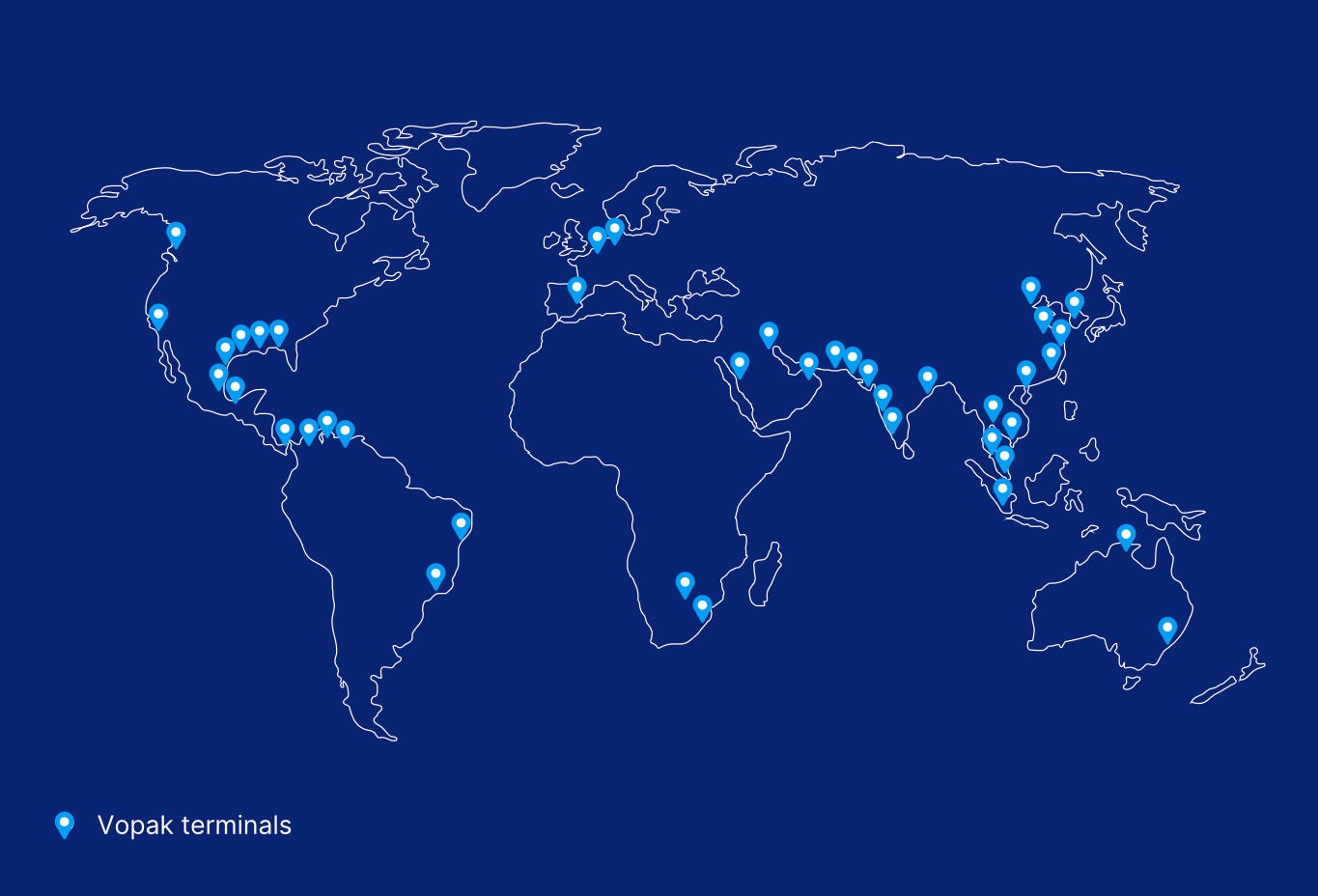

Global Footprint

Vopak has a truly global footprint, operating a network of more than 70 terminals in over 20 countries. The terminals are strategically located in major ports and industrial hubs.

Europe & Africa: the focus is on the storage of oil products, chemicals, and increasingly, new energy carriers. Europe is also a hub for Vopak’s innovation in sustainable storage solutions. The terminals are located in key European ports in Rotterdam, Antwerp, and Hamburg, as well as facilities in Africa.

Asia: Vopak operates a significant network of chemicals, oil, and gas terminals, including Singapore (one of the world’s largest petrochemical hubs), China, India, and the Middle East, serving both local and international markets.

North & South America: the terminals are located in major ports in the United States, Brazil, Mexico, and Panama, with a focus on oil products, chemicals, and gases, supporting both domestic consumption and international trade flows.

Ownership Structure

Vopak's ownership is distributed as follows:

Institutional Investors: the majority of shares are held by institutional investors, including asset managers and pension funds such as BlackRock, APG, and Norges Bank, each with less than 10% ownership.

Stichting Administratiekantoor Vopak: this trust office safeguards company interests and votes on behalf of shareholders. It does not own a significant percentage of shares.

Retail Investors: private individuals hold a small portion of shares.

Treasury Shares: these are held by Vopak for incentive plans and are not eligible for voting or dividends.

Market Overview

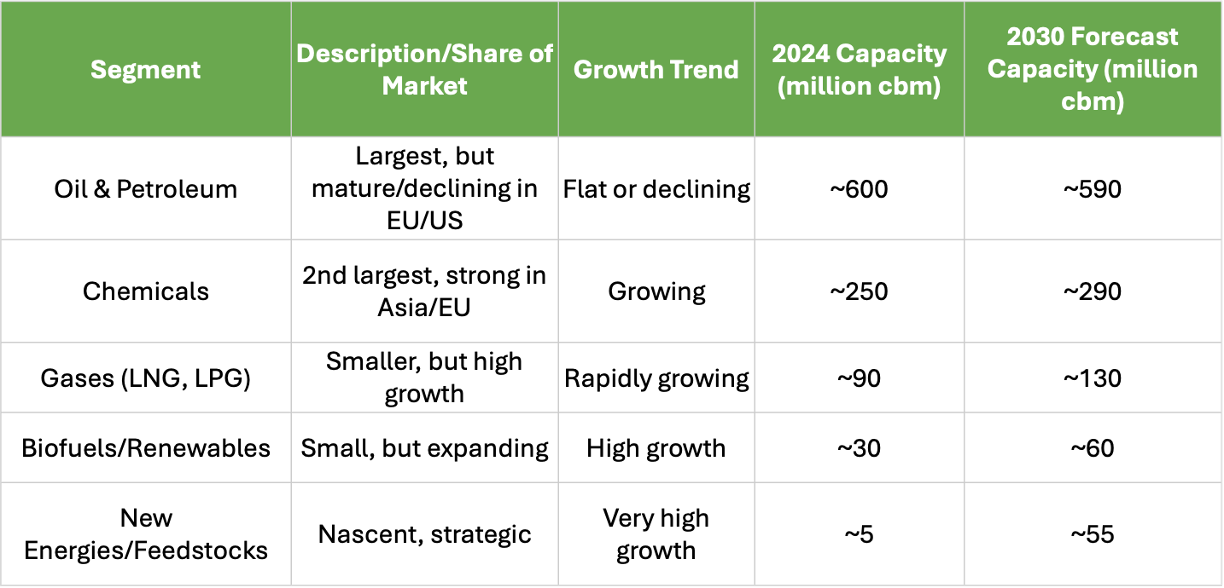

The global tank storage market, which includes the storage of liquid bulk products such as oil, chemicals, gases (LNG, LPG), biofuels, and new energy carriers, has an estimated total capacity of over 1 billion cubic meters worldwide. The global capacity is forecasted to expand further at a CAGR of 1.1% until 2030, with high growth in new energies and chemicals offsetting flat or declining demand for traditional oil storage.

Vopak operates approximately 35.9 million cubic meters of storage capacity, making it the world’s largest independent provider.

The company is present in all segments of the tank storage market.

Market Trends

One of the most important trends to monitor is leasing fees, as most of Vopak's revenue is derived from them. Except for the Oil & Petroleum segment, leasing fee trends are generally favorable.

The storage capacities continue to grow through 2030 in all segments except for the Oil & Petroleum.

The tank storage market is changing fast, driven by the energy transition, shifting trade, and customer needs. Key trends:

Energy Transition: less oil storage, more for chemicals, biofuels, LNG, hydrogen, etc. Vopak's investing in this.

Chemicals Growth: especially in Asia/Middle East. Demand for specialized storage.

LNG Boom: more gas storage needed in Europe/Asia. Vopak's expanding LNG/LPG capacity.

Digitalization: customers want transparency and efficiency. Vopak's investing in smart terminals.

Green Rules: stricter environmental rules favor Vopak's focus on safety and sustainability.

Consolidation: more mergers/partnerships, especially in new energy. Vopak's well-positioned to participate.

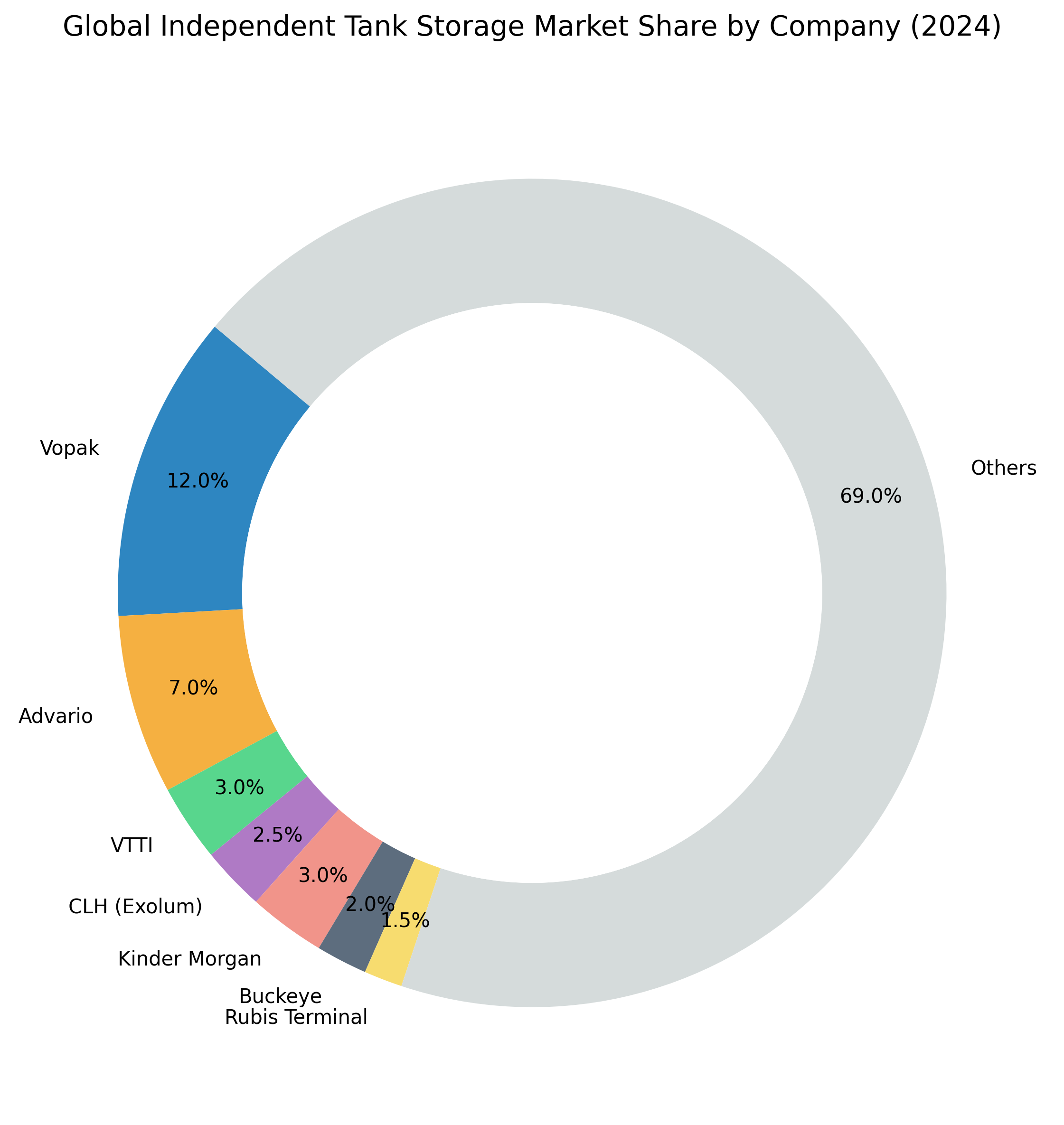

Competitive Landscape

The tank storage market is fragmented, with many local or regional players. There are only a few global players like Vopak.

The main competitors include:

Advario (formerly Oiltanking) (Germany): ~20 million cbm, strong in Europe, Asia, and the Americas.

Royal VTTI (Netherlands/UAE): ~10 million cbm, focus on oil and petroleum, growing in chemicals and gases.

Rubis Terminal (France): ~4.5 million cbm, strong in Europe, focus on chemicals and petroleum.

CLH (Exolum) (Spain): ~8 million cbm, mainly in Europe, focus on oil and refined products.

Kinder Morgan (USA): ~10 million cbm, North America-focused, oil and chemicals.

Buckeye Partners (USA): ~7 million cbm, North America, oil and refined products.

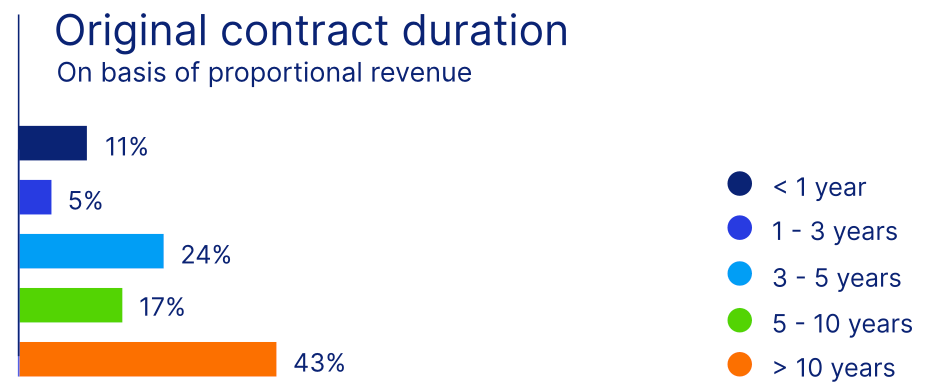

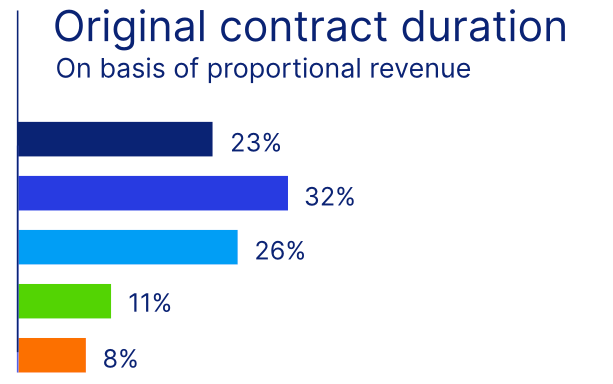

From a business predictability and stability standpoint, contract lengths are important factors. Vopak’s contract portfolio is generally more weighted toward medium- and long-term contracts than the industry average, especially in chemicals, gases, and new energies. This is a key part of Vopak’s strategy to ensure stable, predictable cash flows.

Vopak is the clear global leader in independent tank storage, with the largest capacity, the broadest geographic footprint, and the most diversified product mix.

Deep Dive on Operations

Vopak reports its results by geographical business units, not by product segments. However, I believe insight into the product segments is more valuable so I break it down here.

Gas

The gas segment is one of the fastest-growing contributors to Vopak’s business. The company operates 18 terminals worldwide (both floating and onshore) handling liquefied natural gas (LNG), liquid petroleum gas (LPG), and ammonia.

Vopak’s gas segment accounts for approximately 9% of its total storage capacity (about 3.2 million cbm). The gas terminals operate at high utilization rates due to long-term contracts and strong market demand. The segment’s revenue has grown significantly, especially since 2018, with the expansion of LNG infrastructure in Europe and Asia, now reaching an estimated EUR 240 million (estimated CAGR of 12%).

The majority of the gas storage capacity is contracted on a long-term, take-or-pay basis. This means customers pay for reserved capacity regardless of actual usage, ensuring stable and predictable cash flows for Vopak.

Vopak offers value-added services such as regasification, blending, and transshipment. Many gas terminals are operated through joint ventures, allowing Vopak to leverage local expertise and share investment risks.

Significant expansion projects are underway:

Construction has started on a large-scale (95k cbm) LPG export terminal in Prince Rupert, Western Canada, with an investment of EUR 462 million.

The company is exploring the opportunity to expand the EemsEnergyTerminal in the Netherlands to cater to LNG and potential new energies such as CO₂ and hydrogen.

Industrials

The Industrials segment focuses on providing storage and logistics solutions for refineries, petrochemical plants, and large-scale industrial complexes. These terminals serve as critical infrastructure for feedstock supply, product storage, and integrated logistics and are typically located within or close to industrial clusters. Vopak operates 18 terminals worldwide.

The Industrials segment represents the most significant portion of Vopak’s total capacity, approximately 30–35% of the group’s global storage (approximately 11–13 million cbm). The terminals operate at very high utilization rates (>95%) thanks to their integration with customer operations.

Most industrial terminals operate under long-term (10–20 years), take-or-pay contracts with customers such as refineries, chemical plants, or industrial consortia.

Vopak provides not just storage, but also pipeline connections, product blending, feedstock handling, and in some cases, utility services (steam, nitrogen, etc.), making the terminal an integral part of the customer’s supply chain.

The revenue of the segment is approximately EUR 448 million, with a modest CAGR of approximately 1% since 2018.

As a key strategic pillar, Vopak aims to grow significantly in the Industrials segment and took the following steps in 2024:

Commissioned 560,000 cubic meters of industrial-connected capacity in Huizhou, China.

Expanded its capacities in Saudi Arabia and China, investing EUR 63 million.

Chemicals

The Chemicals segment comprises bulk storage and handling of liquid and gaseous chemical intermediates, solvents, olefins, acids, and specialty chemicals. It is Vopak’s historical core business, dating back to its predecessor companies’ roles in the Rotterdam and Antwerp petrochemical clusters. The terminals operate at very high utilization rates (~95%). The company operates 22 terminals worldwide.

This segment represents the largest single product group in Vopak’s portfolio by capacity (≈ 13–14 million cbm, approximately 38% of the group total). Within this business segment, Vopak serves >600 chemical producers and traders under multi-year contracts.

Vopak has long-term capacity contracts (2–10 years) with take-or-pay commitments (approximately 65% of tanks) and also participates in the short-term/spot business, providing rate upside during tight markets. Because of the higher service intensity and stricter requirements, chemical tanks earn 30–50% higher $/cbm rates than commodity oil storage.

The revenue in this segment has been flat in the last 10 years, totaling approximately EUR 395 million in 2024.

There are several initiatives to stay ahead of the competition:

Rotterdam Chemiehaven expansion (2025-27, +215 k cbm) – for specialty/bio-chemicals.

USGC export debottleneck (Corpus Christi) – adding pipeline manifold and sphere tanks for LPG/LAB feedstocks.

Circular chemicals – pilot tanks for pyrolysis oil, recycled naphtha (Netherlands & Singapore).

Digital twin roll-out to all chemical terminals by 2026, enabling predictive maintenance and real-time customer visibility.

Oil & Petroleum

The Oil segment covers the storage and handling of crude oil, refined petroleum products (gasoline, diesel, jet fuel, fuel oil), and related intermediates. Historically, this was Vopak’s largest segment, but its share has gradually declined due to portfolio shifts toward chemicals, gas, and new energies. The oil segment remains significant, especially in global trading hubs and for strategic storage. Vopak operates 18 terminals worldwide.

The terminals have lower utilization rates compared to gas and chemicals, ranging from 70–95% depending on market cycles. The contracts are more short and medium term.

The revenue in this segment has a cyclical nature and is approximately EUR 421 million, compared to EUR 518 million in 2014.

Vopak has a number of strategic initiatives to maintain its business position:

Portfolio Optimization:

divestment of non-core or underutilized oil terminals in mature markets.

repurposing tanks for biofuels, chemicals, or new energies.

Digitalization:

real-time inventory management, customer portals, and predictive maintenance.

Sustainability:

emissions reduction, vapor recovery, and energy efficiency projects.

Risks

So what are the business risks?

Market: demand for storage is cyclical and sensitive to the economy, energy transition, and customer concentration.

Operational: accidents, aging terminals, and natural disasters can disrupt business and harm reputation.

Regulatory: stricter environmental rules, complex permitting, and ESG demands increase costs and compliance risks.

Financial: the business is capital intensive. There may be high debt needs, rising interest rates, and currency swings that can impact profits.

Competition: increased competition puts pressure margins.

Geopolitical: sanctions, trade barriers, and political instability can disrupt operations.

What is Vopak’s Edge? (Moat)

Vopak has number of differentiating factors:

Prime Locations: hard to replicate, giving access to key trade hubs.

Scale: global reach provides cost advantages and diverse revenue.

Long-Term Contracts: high switching costs lock in customers.

Safety Record: strong reputation attracts customers and reduces risks.

Financial analysis

Vopak’s profitability, cash flow, and capital returns are well above industry averages, though revenue and EVA growth are weak spots. Financial health is solid but liquidity is tight. Management is delivering strong returns and rewarding shareholders, making Vopak a standout in most key areas compared to its peers.

Business quality

Gross margin: Vopak’s gross margin is exceptionally high, especially in the latest period. Industry peers usually post 40–55%. This suggests strong pricing power, a favorable product mix, and operational efficiency.

Net income margin: a net margin near 29% is outstanding—most competitors are in the 10–20% range. This reflects excellent cost control and possibly lower interest or tax expenses.

RoE: above 10% is strong for this sector (industry average: 7–10%). Vopak is using shareholder capital more efficiently than most peers.

FCF margin: this is a real standout — industry FCF margins are typically 15–25%. Vopak’s cash generation is best-in-class, supporting reinvestment and dividends.

Owner earnings margin is well above industry norms, indicating strong underlying profitability and cash flow available to shareholders.

EVA margin is positive but trending down, and is now below the 3–5% typical for top operators. This suggests the spread over the cost of capital is narrowing and that is caused by the high capital investment made by the company.

Growth quality

Revenue growth has been lagging behind the industry average of 2–4% for the last few years. This is due to the shift in business from Oil to Gas and new energy storage segments.

FCF growth is very strong, far outpacing the industry (typically 5–10%). This shows improved cash conversion even as revenue growth lags.

Owner earnings are growing rapidly, well above the sector norm, which is usually in the high single digits.

Financial health

Debt-to-equity (1.10): leverage is moderate and in line with industry norms (1.0–1.5). Vopak is not over-leveraged.

Interest coverage ratio (3.0): coverage is adequate (industry benchmark: 3–5). Vopak can comfortably service its debt, but there’s not a huge cushion.

Current ratio (0.6): below the ideal 1.0, and lower than many peers. Indicates tight short-term liquidity, but not uncommon in capital-intensive infrastructure.

Quick ratio: also lowish, but improving. Still, this is below the 0.7–1.0 seen in more conservative operators.

Management quality

RoA: above the industry average (2–4%), showing efficient use of assets.

ROIC: In line with industry norms (4–6%). Solid, but not exceptional.

CROIC: well above the sector average (5–7%), indicating strong cash generation from investments.

Dividend yield: attractive yield (3.58%), in line with or slightly above the industry average (3–4%).

Share buybacks: consistent buybacks which is shareholder-friendly and better than many peers who rather issue shares to fund growth.

Valuation

The stock’s current price at the time of writing this article is $38.42.

Net assets per share: $26.84

Liquidation value: $57.01

It suggests the stock may be a value stock.

Let’s do the valuation:

expected return (discount rate): 15%

safety margin: 30%

growth rates: I use a starting growth rate of 5% and a terminal growth rate of 1.25%, which is quite conservative provided that the median owner earning growth was 23% in the last 10 years.

With above parameters and after safety margin applied, the intrinsic value would be $41.65 which means a 8% discount.

Verdict

Vopak combines world-class operational quality, a resilient business model, and strong shareholder returns. Its leadership in safety, sustainability, and new energy storage positions it well for the future, even as traditional oil storage declines. While revenue growth is something to pay attention to, the company’s robust cash flow, high margins, and prudent capital management more than compensate.

At current prices, Vopak offers value investors a rare mix of stability, yield, and upside potential. For those seeking a high-quality infrastructure play with exposure to the global energy transition, Vopak is a compelling candidate for consideration.