Resurgence of Oil & Gas - the $26 Trillion Investment Opportunity

Why Oil & Gas Remains Indispensable

In the previous issue I gave an overview about the energy sector as a whole, what is going on, what the trends are. I concluded that fossil (or non-renewable) energy sources are far from being dead and the transition to renewables will take a long time.

In this issue I continue the analysis with the Oil & Gas sector to see where there could be worthy investment opportunities found.

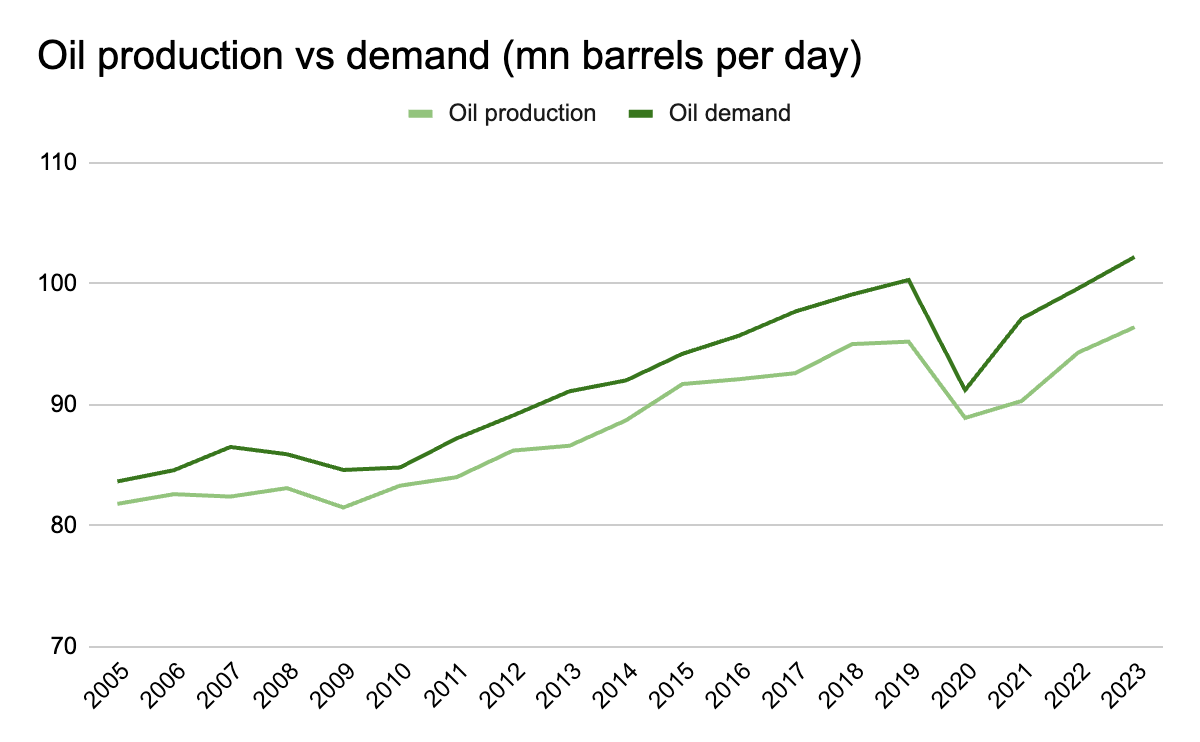

Oil

Source: Statista

Oil demand shows no signs of decline, OPEC forecast says 112.3 mn bpd by 2029 with no peak in demand foreseen. In 2050 OPEC sees 120.1 mn bpd in demand. Other organizations may have different numbers and some estimate peak around 2030 and then flat demand until 2050.

Anyhow, irrespective of which forecast we believe, it seems oil demand will grow steadily at least in the next 5-6+ years.

Road transportation sector is the largest oil consumer representing 49% of the total global demand for oil.

By 2050, there will be 2.9 billion vehicles on the road, 1.2 billion more than in 2023. Despite electric vehicle growth, vehicles powered by a combustion engine will account for more than 70% of the global fleet in 2050.

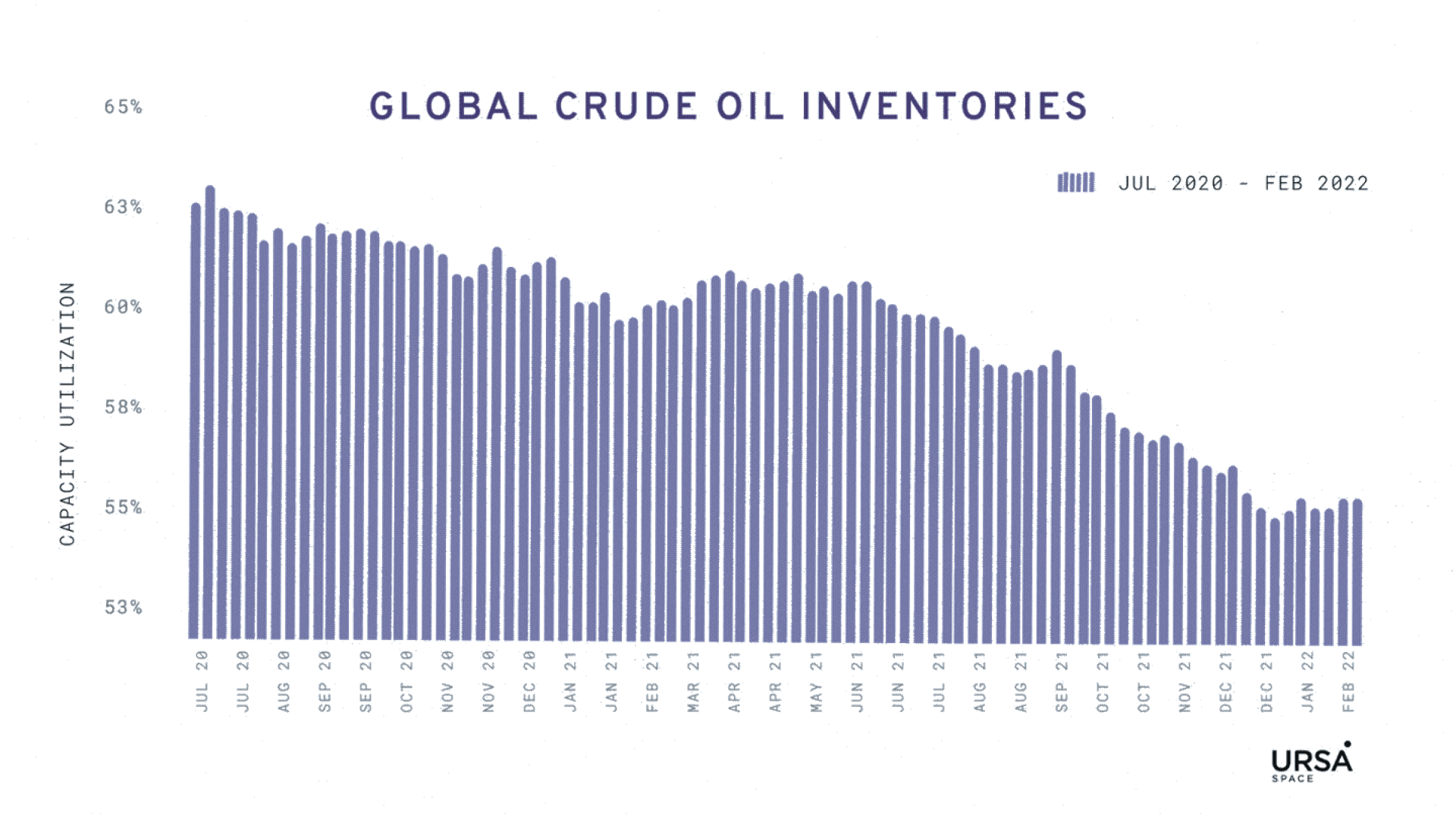

In the meantime the gap between demand and production seems to be widening, which is also reflected in the global crude oil inventories.

Source: URSA

In order to meet demand growth, new projects are needed requiring huge extra CAPEX flow into the industry.

Even if we take the conservative oil demand estimation from Exxon or the different (optimistic) demand scenarios from the International Energy Agency, the need for additional investment is huge.

Source: Exxon

In the last 10 years the investments in the sector showed a declining trend causing major underinvestment. 2023 seems to be a turning point justifying the needed direction above.

The chart below shows the run of the CAPEX for exploration.

Source: Thunder Said Energy

If we look at the whole Oil & Gas upstream industry (exploration + production), annual investment will need to grow to $738 billion by 2030 to ensure adequate supply, which is appx. CAGR 4.5% for the 2025-2030 period. Furthermore OPEC calls for 17.1 trillion investment by 2050, that is huge.

"Expected production declines and future demand growth will require re-investing existing cash flows even as the transition proceeds." - Roger Diwan, Vice-President at S&P Global Commodity Insights

More than 60% of the projected upstream CAPEX increase between 2025-2030 would be focused in the Americas. While the US and Canada are expected to be the largest drivers of CAPEX growth to 2030, Latin America plays an increasingly significant role in non-OPEC supply growth, particularly for conventional crude, with large expansions in Brazil and Guyana and Argentina.

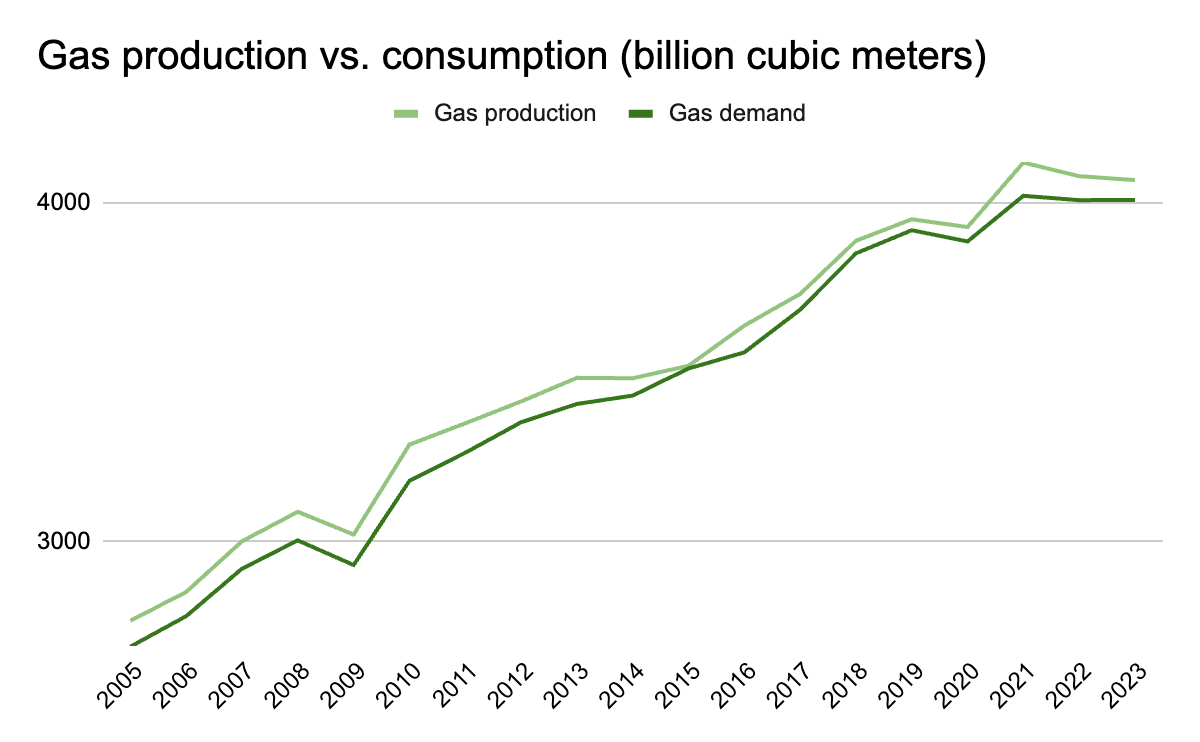

Natural Gas

Source: Statista

Just as for oil, demand seems to be constantly growing until 2050. Most of the consumption goes for power generation.

Source: Gas Exporting Countries Forum

2023 to 2030 CAGR: 1.85%

2030 to 2040 CAGR: 0.96%

2040 to 2050 CAGR: 0.56%

It is not a big surprise. As I wrote in the previous article our electric grids are designed for baseload. Since 2007 natural gas has been gradually displacing coal as a constant baseload power source that is useful for electricity generation. Also natural gas is an ideal “companion” of the renewables: when sun is not shining or the wind is not blowing, natural gas can be “turned on/off” easily. Only natural gas and coal provides such flexibility, you cannot do it with nuclear power. But natural gas surpassed coal as the primary energy source for electricity generation in 2016 and in 2022 it accounted for an estimated 38% of the market.

Above chart assumes that necessary investments would be made for the supply to be able to meet demand. Well, it must definitely happen otherwise…

Source: Exxon

…we would end up in similar situation as with oil.

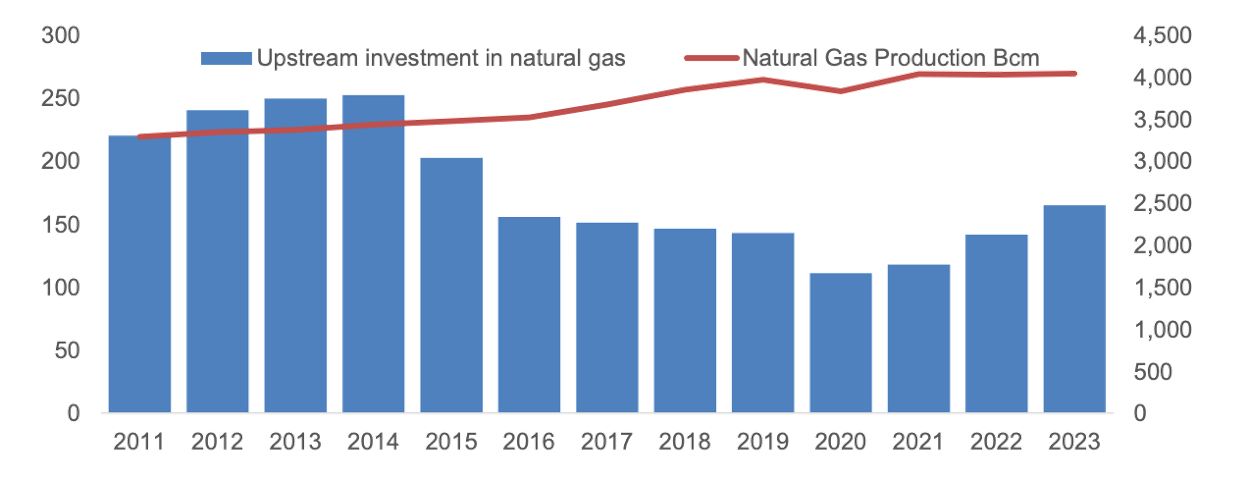

Upstream CAPEX has gradually declined in the 2014-2020 period with a turning point in 2021.

Source: Gas Exporting Countries Forum

The natural gas sector will require 9 trillion USD of investments in the supply chain by 2050.

According to GECF, the Asia Pacific region will receive the largest portion of upstream investments, totalling $2.1 trillion. China, Australia and Indonesia will account for 80% of these investments with China leading the way with $650 billion.

North America forecasted to invest $1.6 trillion, driven by US with $677 billion, followed by Canada with $630 billion.

Investment in Eurasia is estimated to reach $1.5 trillion, with Russia accounting 70% of it.

Africa is set to invest $1.1 trillion, 88% of which will be designated for Algeria, Egypt, Mozambique and Nigeria.

In the Middle East, the anticipated investments will reach of $1.1 trillion, 87% of which will be targeted for Iran, Qatar, Saudi Arabia and the United Arab Emirates.

Latin America and Europe are expected to invest $455 billion and $330 billion, respectively.

Key takeaways

Oil demand show no signs of decline until 2050

Global crude oil inventories are declining

$17 trillion investment required in new exploration and/or production projects to meet increasing demand

Americas will drive the CAPEX growth with Latin America playing an increasingly significant role

Demand for natural gas is increasing up to 2050

Natural gas is the primary source for electricity generation

$9 trillion investment expected in upstream sector until 2050 to meet demands