Oil & Gas: Digging Deeper Than the Headlines

A Comprehensive Look at the Upstream Market: Size, Trends, and Future Outlook

Is Oil & Gas Really Dead? Let’s Look Deeper! 🛢️🔍

A lot of people think the Oil & Gas industry is on its last legs. With the hype around clean energy and renewables, it’s easy to believe that fossil fuels are history. 🌱⚡ But is that really the case?

As I highlighted in my previous article, global demand for oil and gas is actually increasing. Meeting that demand requires massive investment. With this analysis I cut through the noise and take a closer look at the upstream sector.

For the TL;DR version, please scroll to the end.

🏗️ The Value Chain

The upstream sector covers everything from searching for oil and gas to getting it out of the ground. Here’s the breakdown of the activities:

1. Exploration 🗺️

It all starts with the hunt! Companies use geological surveys, satellite images, and seismic studies (think: sending sound waves into the earth and reading the echoes) to find promising spots. If the data looks good, they drill exploration wells to see what’s really down there.

2. Appraisal 🔬

Found something? Time to figure out how big and valuable it is. This means more drilling, more seismic surveys, and lots of testing to estimate how much oil or gas can actually be recovered.

3. Development 🏗️

If the discovery is worth it, the real work begins:

Drilling multiple wells to maximize recovery

Equipping wells for safe, efficient production

Building pipelines, storage tanks, and processing plants

Installing pumps or gas lift systems if needed

4. Production ⛽

Now the oil and gas start flowing! Operations include:

Routine monitoring and maintenance

Well interventions to boost or restore output

Enhanced oil recovery (EOR) techniques like water or gas injection

5. Decommissioning & Abandonment 🚧

When a field is tapped out, it’s time to seal wells, remove equipment, and restore the site to meet environmental standards.

Most oil and gas fields are underground reservoirs containing oil, natural gas, and sometimes water. In case of natural gas, you can hear about:

Associated gas: Natural gas found with oil

Non-associated gas: Gas reservoirs with little or no oil

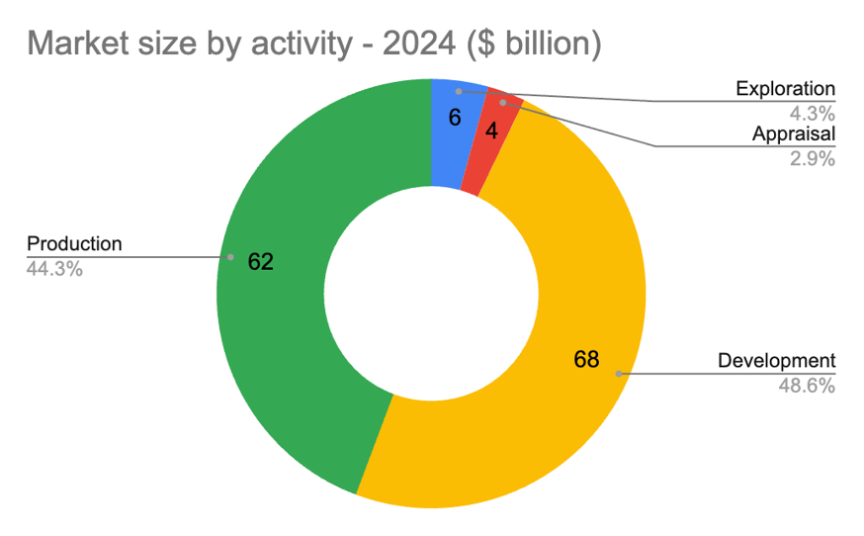

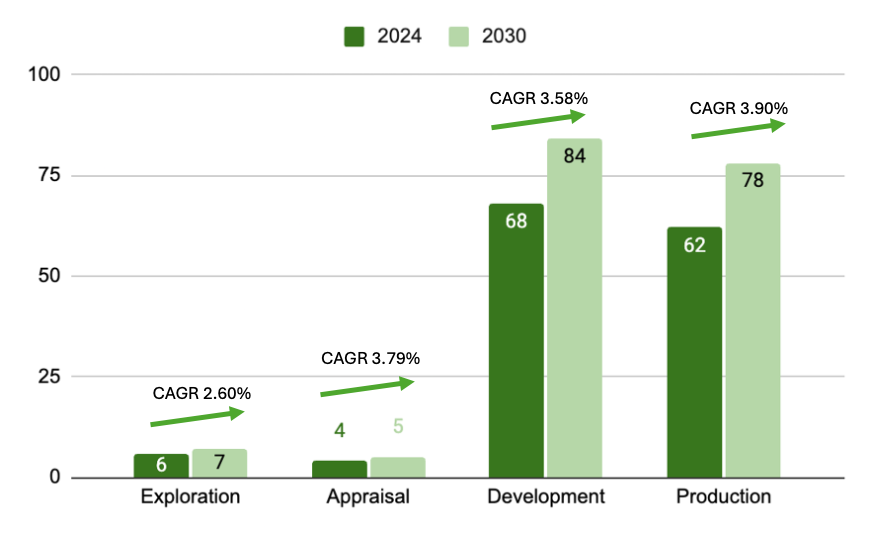

🌍 Market Size & Growth

The upstream oil & gas sector is a $5 trillion market and it’s set to keep growing over the next five years!

The Middle East and North America lead the way in market share.

The market segmentation of the sector is done by various aspects:

Development and Production are the biggest segments, with the fastest growth ahead.

Conventional oil (from traditional drilling) is still the largest segment, but it’s slowly declining.

Non-conventional oil (like shale, oil sands, and extra-heavy oil) and natural gas are growing faster, especially as gas becomes the “bridge fuel” in the energy transition.

Non-conventional natural gas (shale, tight gas, coalbed methane) is expected to grow at a 10% CAGR, while conventional gas will grow at about 3.4% CAGR.

Onshore production dominates, especially for non-conventional resources, while offshore is key for conventional oil and gas.

🌍 Crude Oil Production: Onshore vs. Offshore

About 70–72% of the world’s crude oil comes from onshore fields.

🌏 Major producers: Middle East, Russia, US, China, Canada, Venezuela, Iraq, Iran

Roughly 28–30% of global crude oil is produced offshore.

🌊 Major producers: Brazil, Norway, US (Gulf of Mexico), Angola, Nigeria, UK (North Sea), Mexico, Saudi Arabia (offshore)

🔥 Natural Gas Production: Onshore vs. Offshore

About 77–80% of global natural gas is produced onshore.

🌍 Major producers: US, Russia, Iran, China, Canada, Qatar, Turkmenistan

Appx. 20–23% of natural gas comes from offshore operations.

🌊 Major producers: Qatar (North Dome/South Pars), Norway, Australia, Egypt, Malaysia, UK, Indonesia

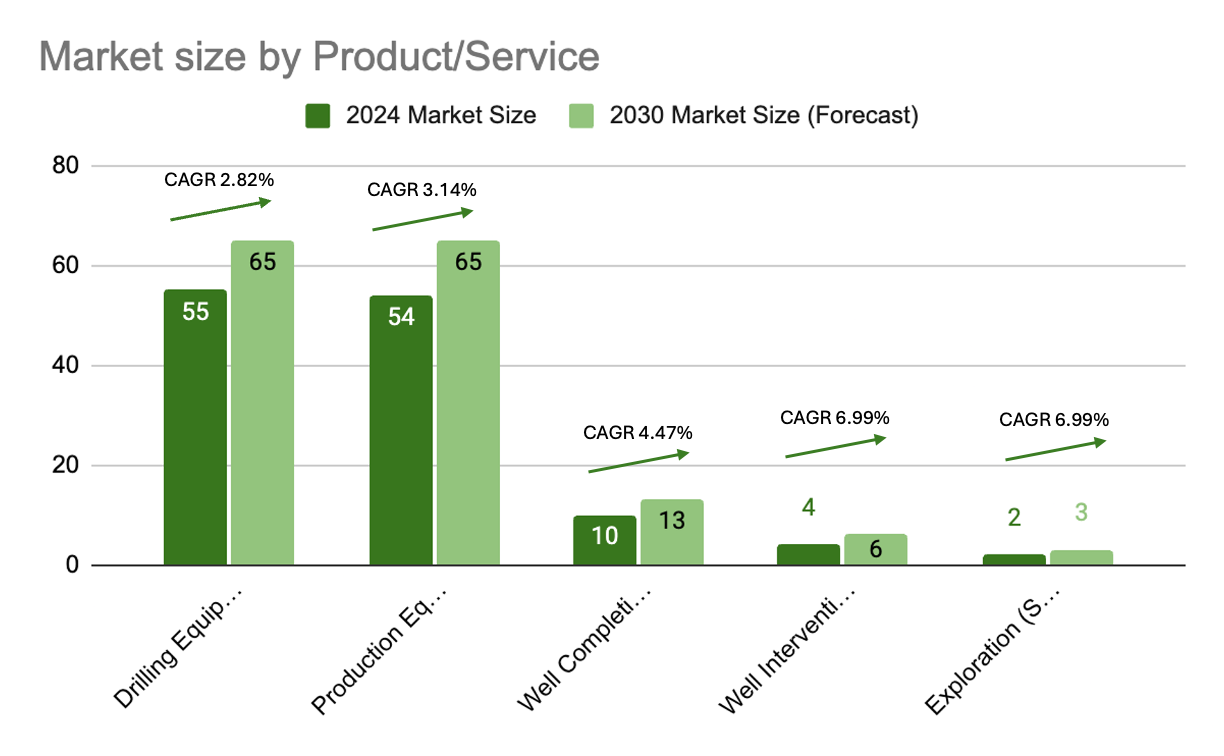

When it comes to industry activity, Drilling Equipment & Services (used during development) and Production Equipment & Services are the two biggest segments—each holding over 40% market share. 🛠️⚙️

Looking at company types:

NOCs (National Oil Companies) are the biggest players, they dominate major producing regions like the Middle East and Russia. 🌏

IOCs (International Oil Companies) are also major forces, operating globally and running large-scale projects. 🌐

Independents are especially important in North American shale, driving innovation and growth. 🇺🇸

OFSCs (Oilfield Service Companies) are on the rise, providing specialised services and cutting-edge technology to all the other players. 🚀

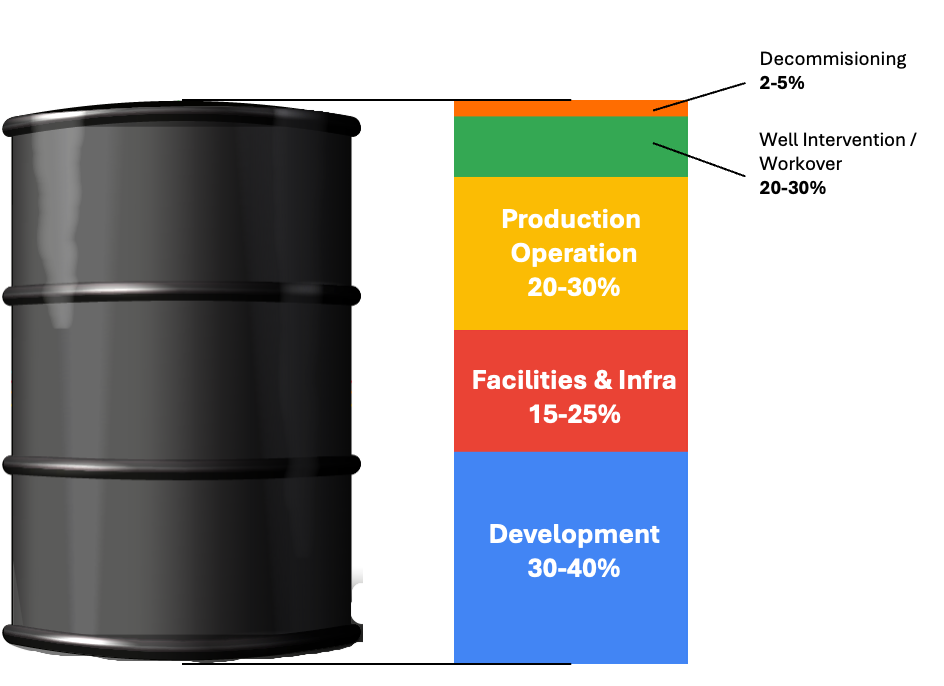

💸 Economics: What Does It Cost?

Cost structure

Upstream oil & gas is capital-intensive. Here’s the breakdown of cost elements:

Capex: Upfront costs for exploration, drilling, and infrastructure

Opex: Ongoing costs for production, maintenance, labor, and energy

Decommissioning: End-of-life costs for plugging wells and restoring sites

The typical cost structure per barrel of oil looks like this (for conventional onshore oil):

Production cost

Production costs vary by region. OPEC countries (mainly the Middle East) have the lowest costs, giving them a big advantage and market power.

Profitability and payback period

Breakeven prices range from under $20/bbl (Middle East) to $40–60/bbl (shale, deepwater, oil sands).

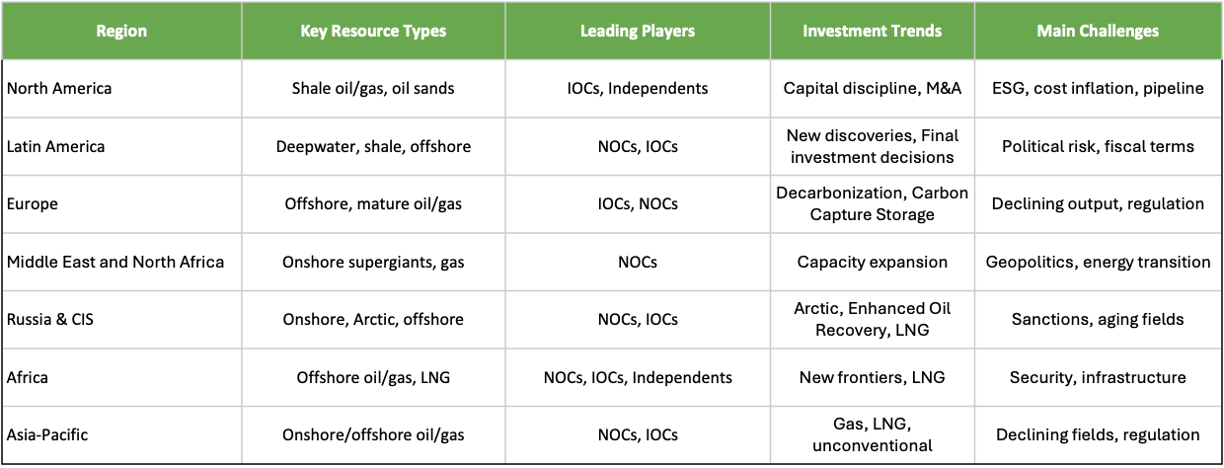

🏢 Who’s Who in the Industry? - Key players

National Oil Companies are controlling most of the resources. A comparison by company types side-by-side:

National Oil Companies are the heavyweights in the Middle East and Russia, while North America is the “playground” of the Independents. Europe and Latin America are bit more balanced with a healthy mix of NOCs, IOCs, and Independents all competing for market share.

A snapshot of the scene showing which regions are rich in resources, who the key players are, where the money is flowing, and what challenges each area faces. Every region has its own strengths and hurdles, making the energy market a truly dynamic and diverse space.

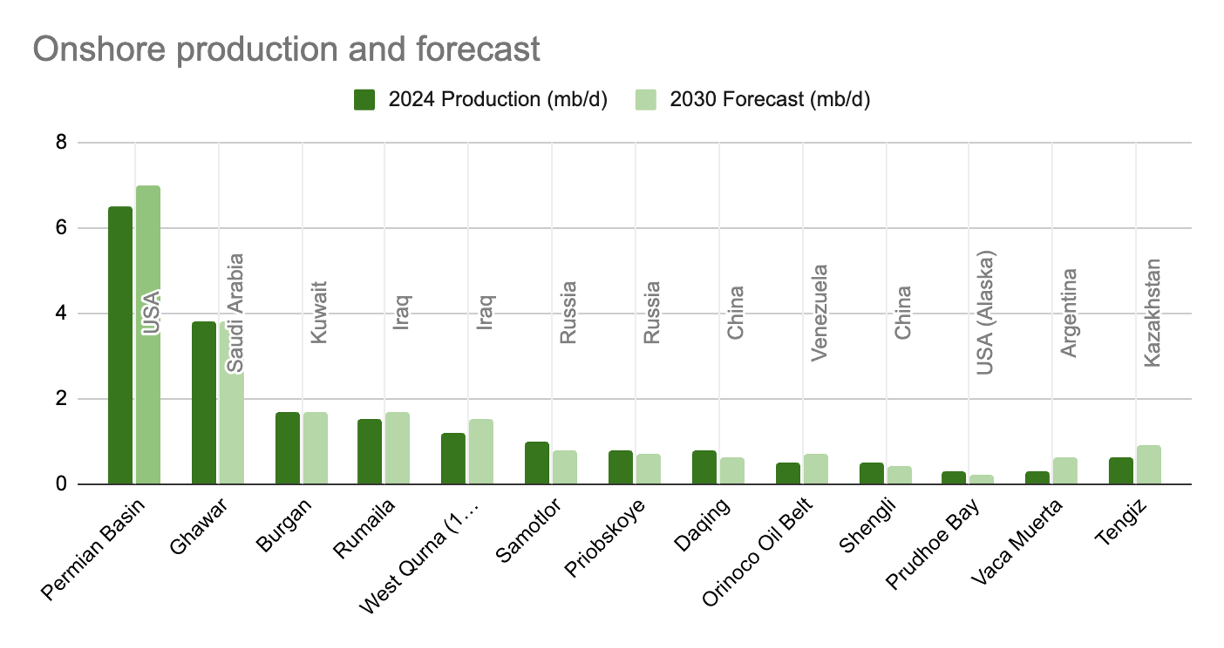

🌎 Where’s the Action? Major Fields & Hotspots

The largest production sites in the world, onshore and offshore.

Onshore: Growth is slowing, but big projects are underway in the U.S., Argentina, and Kazakhstan. The Permian Basin’s best fields are depleting, so less-productive sites are next.

Offshore: Growing fast, especially in Latin America, West Africa, and Asia Pacific. By 2030, offshore could make up 37% of global production (compared to 29% in 2024).

Site expansions and new projects are needed to meet global oil demand and to balance out the declining, maturing production.

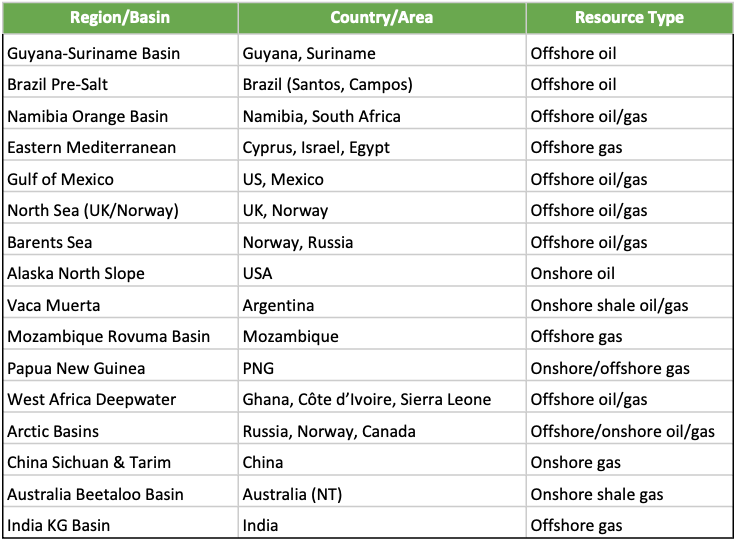

Largest exploration & appraisal sites (2024-2025)

Exploration Hotspots (unexplored or underexplored regions):

Onshore: The Arctic, Central Africa, South America’s Amazon Basin, and the Middle East’s Rub’ al Khali

Offshore: Namibia/Angola, Suriname-Guyana Basin, Eastern Mediterranean, Brazil’s Equatorial Margin, and the U.S. Gulf of Mexico (ultra-deepwater)

Reasons for these areas being un(der)explored are harsh conditions and logistics challenges (e.g. Arctic), technical and cost barriers (e.g. U.S. Gulf ultra-deep water) or environmental / political contraints (e.g. Orinoco Belt extensions, Amazon Basin).

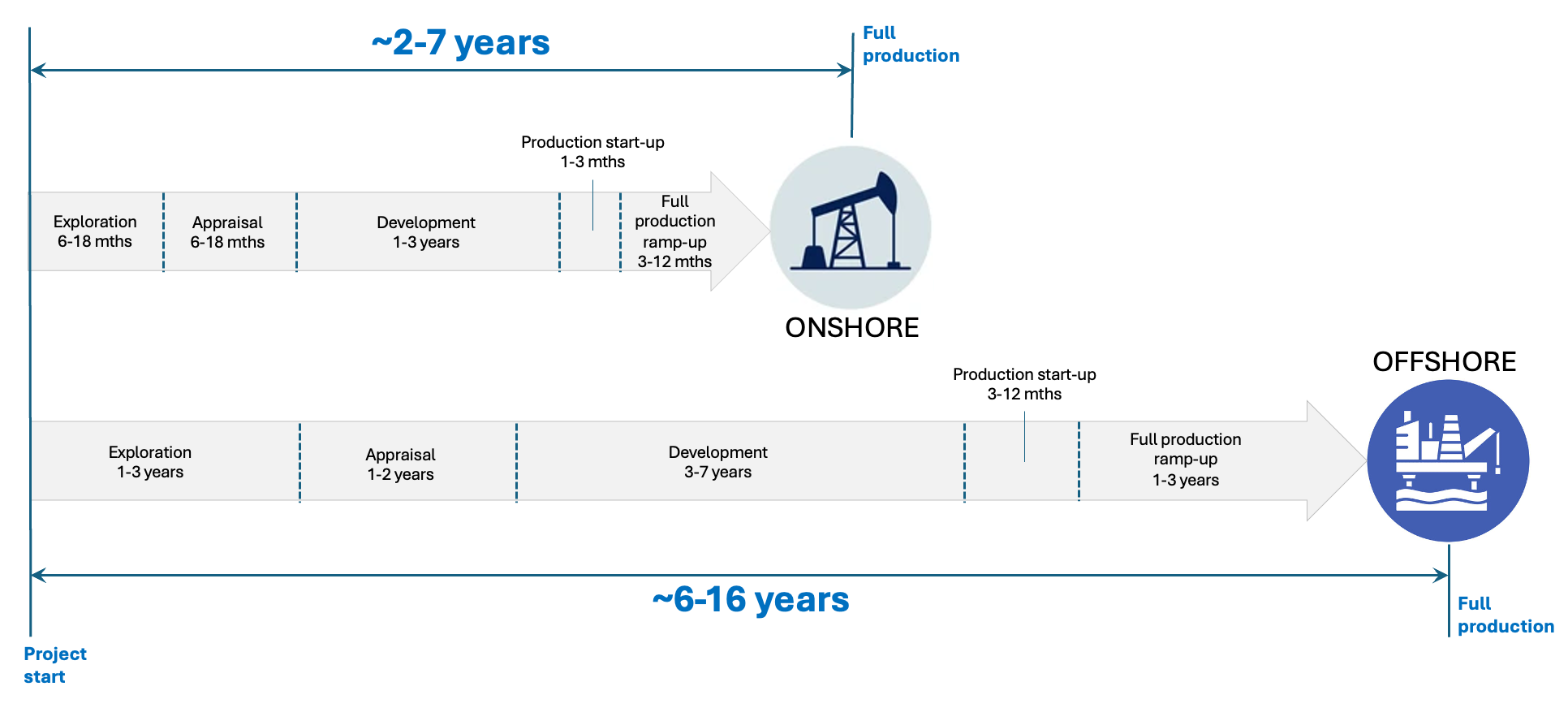

New projects have long lead times. Offshore projects take much longer to develop, but - as said - they’re crucial for future supply.

📈 Market Drivers & Challenges

What’s driving the market?

Global energy demand: Population growth and industrialization, especially in Asia and Africa

Petrochemical demand: Oil & gas are essential for chemicals, even as transport electrifies

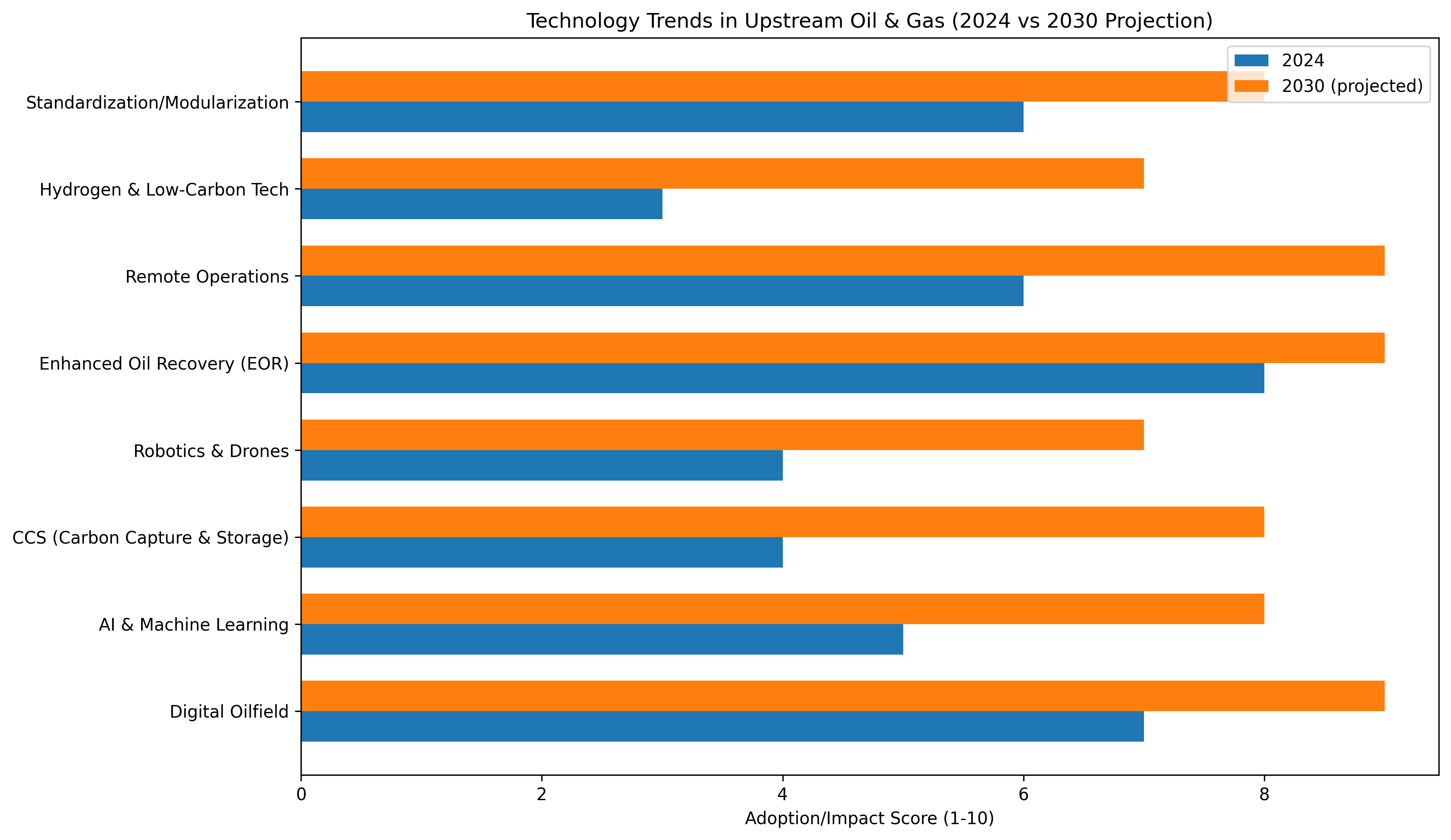

Tech advances: Digitalization, AI, and enhanced oil recovery are making operations smarter and more efficient

Favorable policies: Tax breaks, new licensing rounds, and supportive regulations

Geopolitics: OPEC+ decisions, resource security, and supply disruptions all move the market

Energy transition: Natural gas is the “bridge fuel,” and LNG demand is booming

Right now we are in the expansion phase of the market cycle with high capex, and service sector tightness.

What are the challenges?

Price volatility: Oil & gas prices swing wildly, making planning tough

High costs: Deepwater and unconventional projects are expensive

Regulation: Stricter environmental rules and longer permitting times

ESG pressures: Investors and the public want lower emissions and better social performance

Resource maturity: Many giant fields are declining, new discoveries are critical

Geopolitical risks: Political instability, sanctions, and conflicts can disrupt supply

🔮 The Road Ahead: Trends & Outlook (2024–2035)

Oil & gas will remain essential for transport, industry, and chemicals through 2050

Natural gas demand will grow fastest, especially in Asia and for LNG exports

Deepwater, LNG, and unconventional resources will drive new supply as mature fields decline

Emerging markets and frontier basins (Brazil, Guyana, Namibia, East Africa) are attracting big investment

ESG and decarbonization: Carbon capture, methane reduction, and renewables are becoming standard

Digitalization: Real-time data, AI, and automation are boosting efficiency and safety

M&A and partnerships: Companies are joining forces to share risk and accelerate innovation

Cost discipline: Focus is shifting to profitability, cash flow, and capital efficiency

TL;DR

Oil & Gas Remain Essential: Despite the hype around renewables, global demand for oil and gas is still rising, driven by population growth, industrialization, and the ongoing need for petrochemicals and transport fuels.

Massive Market, Ongoing Growth: The upstream oil & gas sector is a $5 trillion industry, with the Middle East and North America leading in market share. Development and production are the largest and fastest-growing segments.

Onshore Still Dominates, But Offshore Is Rising: About 70–72% of oil and 77–80% of natural gas are produced onshore, but offshore projects—especially in Latin America, West Africa, and Asia Pacific—are growing rapidly and will be crucial for future supply.

Diverse Players, Global Reach: National Oil Companies (NOCs) control most resources in the Middle East and Russia, while Independents drive innovation in North America. International Oil Companies (IOCs) and Oilfield Service Companies (OFSCs) play vital roles worldwide.

Capital-Intensive, Cost-Driven: Upstream projects require huge upfront (capex) and ongoing (opex) investments. Production costs vary widely, with the Middle East enjoying the lowest costs and highest profitability.

Major Fields & Hotspots: The world’s largest oil and gas fields are concentrated in a few regions, but new exploration is targeting frontier areas like Guyana, Namibia, the Arctic, and deepwater basins.

Market Drivers: Key growth factors include global energy demand, petrochemical needs, technological advances, favorable policies, and the role of natural gas as a “bridge fuel” in the energy transition.

Challenges Remain: The industry faces price volatility, high costs for complex projects, stricter regulations, ESG pressures, resource maturity, and geopolitical risks.

Future Outlook: Oil & gas will remain critical through 2050, with natural gas demand growing fastest. Deepwater, LNG, and unconventional resources will drive new supply. Digitalization, decarbonization, and strategic partnerships are shaping the next era.

Bottom line: Oil & gas are far from dead. The industry is evolving, investing, and innovating to meet global energy needs—while navigating new challenges and opportunities in a changing world.

Incredible write up giving a very clear overview of the oil & gas landscape. Would be interesting to understand how you approach the sector as an investor.