Gold Rush 2.0: The Best Is Yet To Come

Why the Bull Run is Just Getting Started

Gold has been the ultimate safe haven for centuries. Through wars, economic crises, and inflationary periods, it has stood the test of time as a reliable store of value. When the world gets shaky — whether it’s geopolitical tensions, currency devaluations, or financial turmoil — investors turn to gold for stability.

It’s a timeless asset that never goes out of style.

Gold is money. Everything else is credit. - J.P. Morgan

Gold has protected purchasing power for generations, proving its worth time and time again.

Source: World Gold Council. Prices indexed at 100 in 1930

Fast forward to today, and we’re once again in turbulent times. Gold has surged from around $2,000 to $3,000 in just a year — a solid 50% jump.

But the big question is: Is there still room for more growth?

If you’ve missed the rally so far, is it too late to jump in?

I believe the real “gold squeeze” is just getting started and could last until the end of 2026.

Here are 5+1 reasons why gold’s bull run still have plenty of steam left.

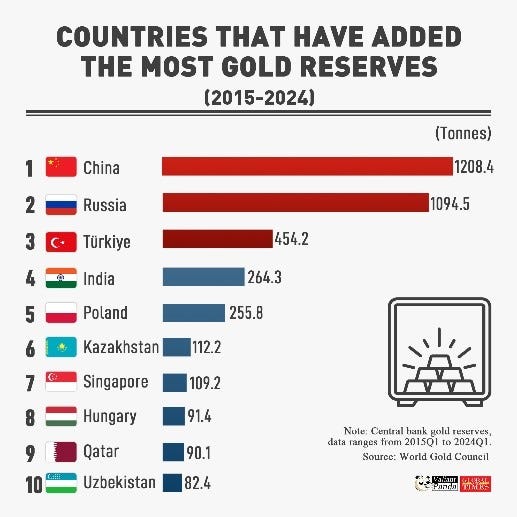

1. Demand By Central Banks Remains Strong

Central banks have been the driving force behind gold demand for over a decade. Since 2008, they’ve flipped from being net sellers to net buyers…

..and their gold reserves have grown significantly.

Source: Bloomberg finance

Today, we are again in a complex geopolitical and financial environment. Accumulating gold is more relevant than ever.

There is no stopping of stockpiling gold by central banks. Now around 18% of all the gold ever mined is held by central banks.

Source: World Gold Council

Even the U.S., which has the largest gold reserves globally, is under pressure to rethink its gold policy as its reserves are at their lowest levels in 90 years.

Source: Trading Economics

Meanwhile, other countries (e.g. India, Turkey) are issuing bonds backed by gold, with trading volumes hitting $50 billion in early 2025 and is growing.

2. Shifting G7 vs. BRICS dynamics

The sanctions - coordinated by the U.S. and the E.U. - on Russia in 2022, including freezing $300 billion in assets and banning the country from SWIFT, triggered a major shift and especially the BRICS nations (or those who were reluctant to apply the sanctions) have accelerated their gold purchases.

Due to the sanctions and economic inequality, the BRICS countries are working on creating a new currency system partially backed by gold.

This would be a “big bang” considering that the BRICS economic power is now comparable to the G7 and and a gold-backed currency would challenge the dominance of the U.S. dollar.

4. Institutions and Retail Investors Are Joining the Party

Finally in Q1 2025 institutions, hedge funds and retail investors also started to turn to gold and significantly increased their holdings during 2025 Q1.

This could be a catalyst to gold prices now that the the demand is driven not only by central banks.

5. Stronger Fundamentals Than Earlier

Compared to the last two bull runs in 2011 and 2020, the fundamentals are stronger.

Source: Bloomberg, World Gold Council

U.S. gold ETF buyers have been on the sidelines as gold ETFs are a smaller share of total ETF assets, leaving room for more growth.

Real yields are higher, which historically supports gold prices.

Stock market valuations remain high, with downside pressure that could drive more investors toward gold.

The dollar, while still strong, is facing headwinds, including tariff uncertainties and a push for a weaker currency by the Trump administration.

Some history -gold prices, rally returns and their durations

Source: Bloomberg, World Gold Council

On the supply side, gold supply hit an all-time high of 3,661 tons in 2024, but it’s expected to peak by late 2025 or early 2026. Beyond that, a supply crunch could emerge as new gold discoveries have plummeted.

+1 US potential revaluation of their gold reserves

As I wrote in this article, U.S. debt level is at an unsustainable level ($35 trillion).

There is a major headache: between January and June 2025, $9.2 trillion will mature, which is roughly twice the total annual federal income.

Source: The Kobeissi Letter / X

Issuing new bonds would be extremely expensive given the current interest rate that is the highest in the last 15 years. Fast and significant rate cuts are not likely, other alternatives needed.

“We’re going to monetize the asset side of the U.S. balance sheet.” - Scott Bessent, U.S. Treasury Secretary

While various assets could be monetized, gold has captured the market’s attention.

U.S. is having the largest gold reserve in the world.

It has been in the balance sheet since 1973 with a valuation of just $42 per ounce.

Revaluing it at current market price would mean an addition $700-800 billion to the balance sheet that could be used to:

Pay down existing debt

Fund new government programs

Create a sovereign wealth fund

Build additional strategic reserves

Such a move would be a massive bullish signal for gold, potentially triggering a domino effect as other central banks follow suit. Analysts predict this could lead to a 50-200% price increase, creating a bubble in metals over time.

If history is any guide, gold’s role as a safe haven isn’t going anywhere. And with all these factors in play, the next few years could be golden for investors.

Key takeaways

Central banks have been net buyers of gold since 2008.

BRICS nations are working on a gold-backed currency to rival the U.S. dollar.

Institutions and retail investors are increasingly turning to gold.

Current market fundamentals are stronger than during the last two bull runs (2011, 2020).

A supply crunch is expected beyond 2025.

A potential revaluation of U.S. gold reserves could send prices soaring.