Add to your watchlist #4: Monolithic Power Systems

Every week, I hunt through global markets looking for companies that make me take notice.

I find plenty of fantastic businesses with rock-solid fundamentals. But right now they're just too expensive based on my valuation standards. So instead of jumping in, it's wiser to add them to your watchlist and wait for a better price.

Let's talk about this week's standout company.

Monolithic Power Systems Inc.

Symbol:

MPWRCountry: United States

Listed: NASDAQ

Market cap: $32.8bn

Price: $685.90 (2025-06-20)

Monolithic Power Systems, Inc. (MPWR) is a US-based semiconductor company founded in 1997 and headquartered in Kirkland, Washington. MPWR designs, develops and markets high-performance power solutions for a wide range of industries. The company is listed on the NASDAQ under the ticker MPWR and has become a favorite among growth investors due to its consistent execution and focus on innovation.

What does MPWR do? Products and revenue streams

MPWR specializes in analog and mixed-signal integrated circuits (ICs) with a core focus on power management solutions. Their chips are used to efficiently convert, regulate and manage electrical power in electronic devices. Here’s a breakdown of their main product lines and revenue streams:

DC-DC power conversion ICs: these chips are the backbone of MPWR’s business, used in everything from laptops and servers to industrial equipment. They help convert one voltage level to another with high efficiency, which is critical for battery-powered and energy-sensitive devices.

Lighting control ICs: MPWR provides solutions for backlighting in LCD displays, automotive lighting and general LED lighting. This segment is growing as LED adoption increases globally.

Motor drivers: these ICs control motors in applications like automotive systems (think electric power steering), industrial automation and consumer electronics.

Battery management ICs: used in portable devices, power tools and electric vehicles, these chips help monitor and optimize battery performance and safety.

Other analog ICs: MPWR also offers a range of sensors, interface ICs and other analog components that complement their power management portfolio.

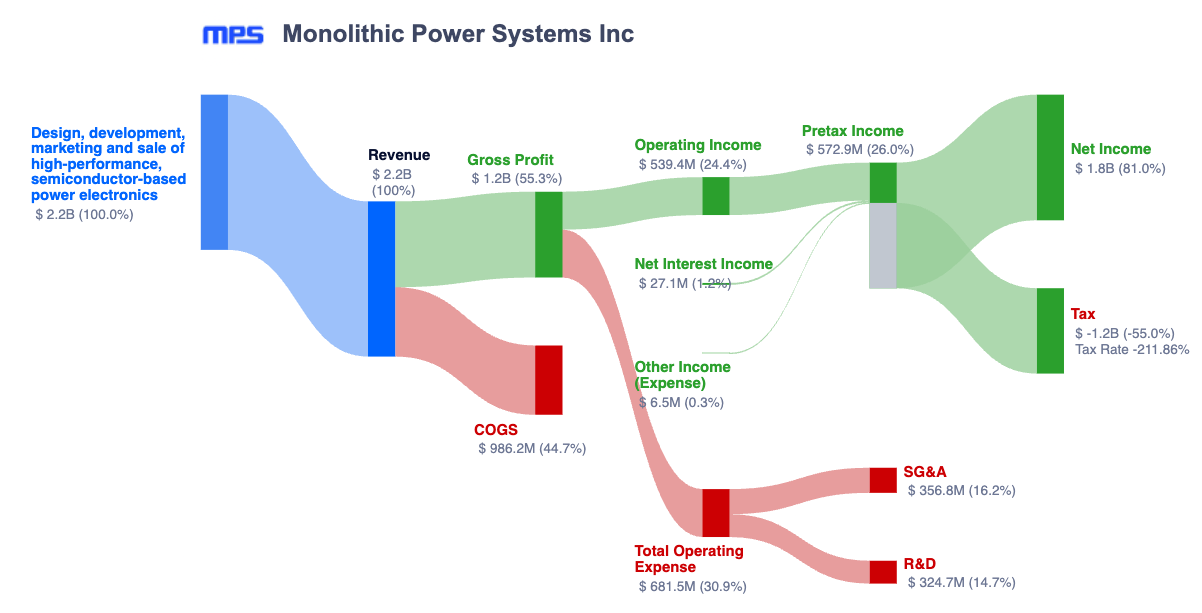

In 2024, MPWR reported total revenues of about $2.2 billion. The largest revenue contributors were the Computing & Storage segment (serving data centers and cloud infrastructure) followed by Automotive, Industrial and Consumer segments. The company’s customer base is well-diversified, with no single customer accounting for more than 10% of revenue, which reduces concentration risk.

Market trends and outlook

The power management IC market is expected to see robust growth through 2030 driven by several secular trends:

Data center and cloud growth: the explosion of AI, cloud computing and edge devices is fueling demand for efficient power solutions in servers and storage. MPWR is well-positioned here, as hyperscale data centers require more power-efficient chips to manage rising energy costs.

Electrification of vehicles: the shift to electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is a huge tailwind. MPWR’s automotive segment is growing fast, with design wins in EVs, infotainment and safety systems.

Industrial automation and IoT: as factories and infrastructure become smarter, demand for reliable, efficient power management increases. MPWR’s industrial segment benefits from this trend.

Consumer electronics: while this market is more cyclical, the proliferation of smart devices, wearables and portable gadgets keeps demand steady for battery management and power conversion ICs.

LED lighting: global energy efficiency initiatives and the shift to LED lighting continue to support MPWR’s lighting control business.

On the flip side, the semiconductor industry is cyclical and exposed to inventory corrections, trade tensions and supply chain disruptions. However, MPWR’s fabless model (outsourcing manufacturing) and focus on high-value, niche applications help cushion some of these risks.

The numbers that matter

Exelixis has an nice gross margin of 55.4%. In Q1 2025, their net income margin hit 20.99%. Not bad at all.

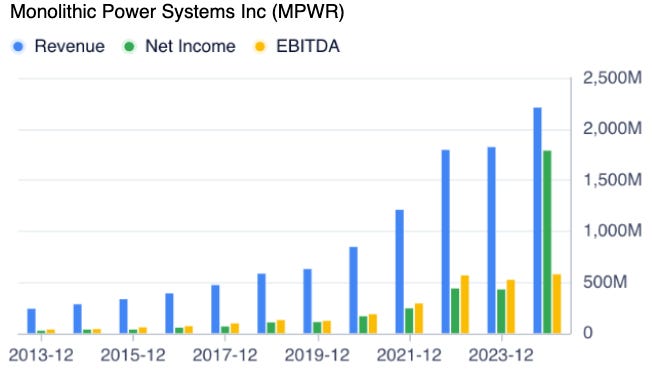

Revenue growth has been steady over the past five years with a 28.58% CAGR. That's solid, consistent expansion without any dramatic ups and downs.

Their free cash flow margin was outstanding at 33.89% in Q1 2025. Their 10-year average is also impressive, 20.34%. This company generates serious cash.

The free cash flow growth was awesome at 39.98% CAGR over five years.

Their return on invested capital (ROIC) was 15.36% over the last 5 years and their cash-adjusted ROIC hit 19.94%. Those are eye-popping numbers that show how efficiently they're using shareholder money.

My take

MPWR stands out for its strong engineering culture, diversified end markets and consistent execution. The company’s focus on high-growth areas like data centers and EVs, combined with a robust product pipeline, gives it a solid runway for growth. I think the secular trends in electrification, cloud and automation are all working in MPWR’s favor and their track record of innovation makes them a compelling pick for long-term investors. Just keep in mind, the stock isn’t cheap and the sector can be volatile, so patience is key.

Interesting.

BTW I sent you a DM regarding more info about your portfolios