Add to your watchlist #3: Exelixis

Every week, I hunt through global markets looking for companies that make me take notice.

I find plenty of fantastic businesses with rock-solid fundamentals. But right now they're just too expensive based on my valuation standards. So instead of jumping in, it's wiser to add them to your watchlist and wait for a better price.

Let's talk about this week's standout company.

Exelixis, Inc.

Symbol:

EXELCountry: United States

Listed: NASDAQ

Market cap: $11.3bn

Price: $41.59 (2025-06-13)

Exelixis is a biopharmaceutical company that's all about finding, developing and selling new medicines for really tough cancers. Founded back in 1994, they have come a long way from being a genomics research shop to actually having cancer drugs on pharmacy shelves.

What Exelixis does

Think of Exelixis as cancer detectives. They hunt down specific molecular targets that fuel cancer growth, then design small molecule drugs to shut them down. It's not the “spray-and-pray” approach of traditional chemotherapy. Instead, they're going after cancer's specific weak spots.

Their process is pretty straightforward: find promising drug candidates, test them in clinical trials and if they work, get them to patients who need them.

The money makers

Exelixis has built their business around a few key products, mainly targeting kidney, liver and thyroid cancers:

Cabometyx (cabozantinib): this is their superstar. Cabometyx blocks multiple pathways that cancer cells use to grow and spread. It's approved for advanced kidney cancer, liver cancer and a rare type of thyroid cancer. The drug works by jamming the signals that tell tumors to build new blood vessels and metastasize.

Cometriq (cabozantinib): same active ingredient as Cabometyx, but formulated differently for a specific type of thyroid cancer.

Pipeline products: the company not sitting still, but they keep investing in new therapies and finding new uses for their existing drugs.

The licensing game

Here's where it gets interesting. Exelixis doesn't just make money selling pills directly. They've got licensing deals with other pharmaceutical companies that bring in serious cash.

They have partnered with companies like Ipsen and Takeda to sell Cabometyx outside the US. These deals work like this: Exelixis gets upfront payments, milestone bonuses when certain goals are hit and then ongoing royalties from sales. It's like getting paid three different ways for the same product.

This licensing strategy is smart because it gives them multiple revenue streams to fund their research without having to build sales teams in every country.

This is the breakdown of how Exelixis is making money:

Market trends working in their favor

Several big trends are playing in Exelixis's favor:

Precision medicine: doctors increasingly want treatments tailored to each patient's specific cancer genetics. Exelixis's targeted approach fits perfectly here.

Combination therapies: there's growing excitement about combining targeted drugs like Cabometyx with immunotherapies. Early trials suggest these combos might work better than either treatment alone.

Rising cancer rates: unfortunately, cancer cases are climbing globally as populations age. More patients means more demand for effective treatments.

Faster approvals: regulators are speeding up approval processes for promising cancer drugs, which could help Exelixis get new treatments to market quicker.

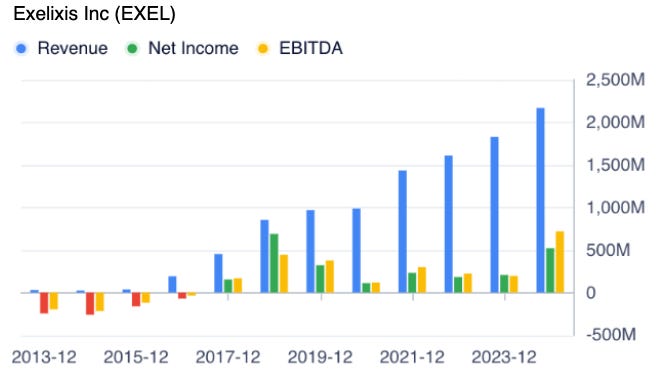

The numbers that matter

Exelixis has an incredible gross margin of 96%. That means for every dollar of revenue, they keep 96 cents after direct costs. In Q1 2025, their net income margin hit 28.74%. Not bad at all.

Revenue growth has been steady over the past five years with a 17.51% CAGR. That's solid, consistent expansion without any dramatic ups and downs.

Their free cash flow margin was outstanding at 38.07% in Q1 2025. Even more impressive? Their 10-year average is actually higher at 39.08%. This company generates serious cash.

The free cash flow growth was more moderate at 4.27% CAGR over five years, but still positive.

Here's where things get really interesting: their return on invested capital (ROIC) was 78.89% in Q1 2025 and their cash-adjusted ROIC hit 112.99%. Those are eye-popping numbers that show how efficiently they're using shareholder money.

My take on Exelixis

Here's what I think about EXEL: it's a fundamentally strong company in a growing market. Their focus on targeted cancer therapies puts them right in the sweet spot of where medicine is heading. The licensing deals provide steady income streams that fund their research pipeline.

Financially, the numbers look great. High margins, consistent growth, strong cash generation and incredible returns on capital.

But even great companies can be overpriced, like this one.

I'd rather suggest adding EXEL to your watchlist and waiting for a better entry point.

The oncology market isn't going anywhere and neither is Exelixis's competitive position. Sometimes the best investment decision is knowing when not to buy, even when you love the company.

Well, that's my take on Exelixis. A solid company in a growing market, but patience might pay off for those willing to wait for the right price.